A string of three losing trades can feel like a confirmation bias feeding on every market twitch, especially when currency swings amplify position size overnight. For many Nigerian traders the pain isn’t just capital lost — it’s the way volatility turns a rational plan into emotional decisions that compound risk.

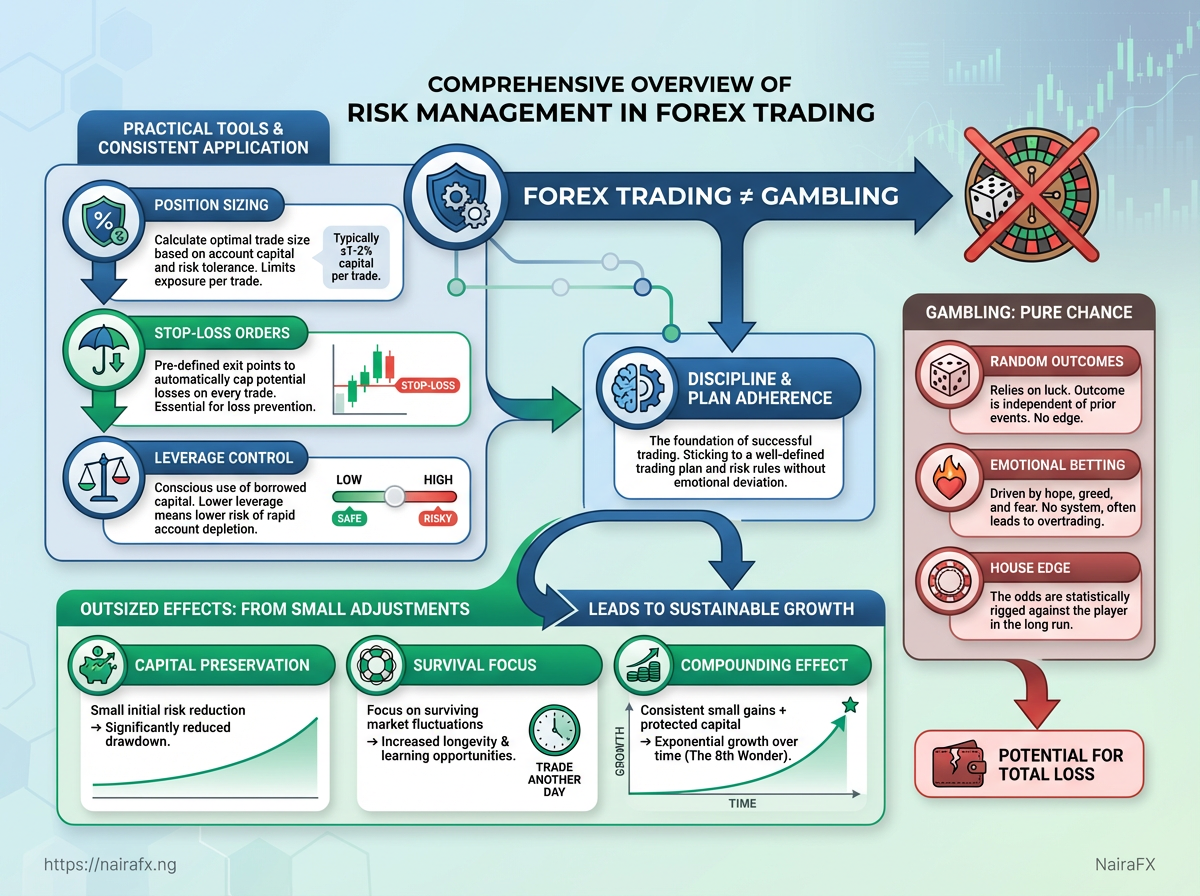

Effective risk management reduces those moments where one trade wrecks a month of progress. Practical tools such as position sizing, stop-loss placement and prudent use of leverage aren’t theoretical rules to memorize; they are tactical instruments that change the odds in your favor when applied consistently.

Beyond tools, the discipline to follow a risk plan separates casual gamblers from repeatable traders. Small adjustments to capital at risk and trade frequency produce outsized effects over weeks, and understanding that math makes trading less about prediction and more about surviving to trade another day.

Executive Summary

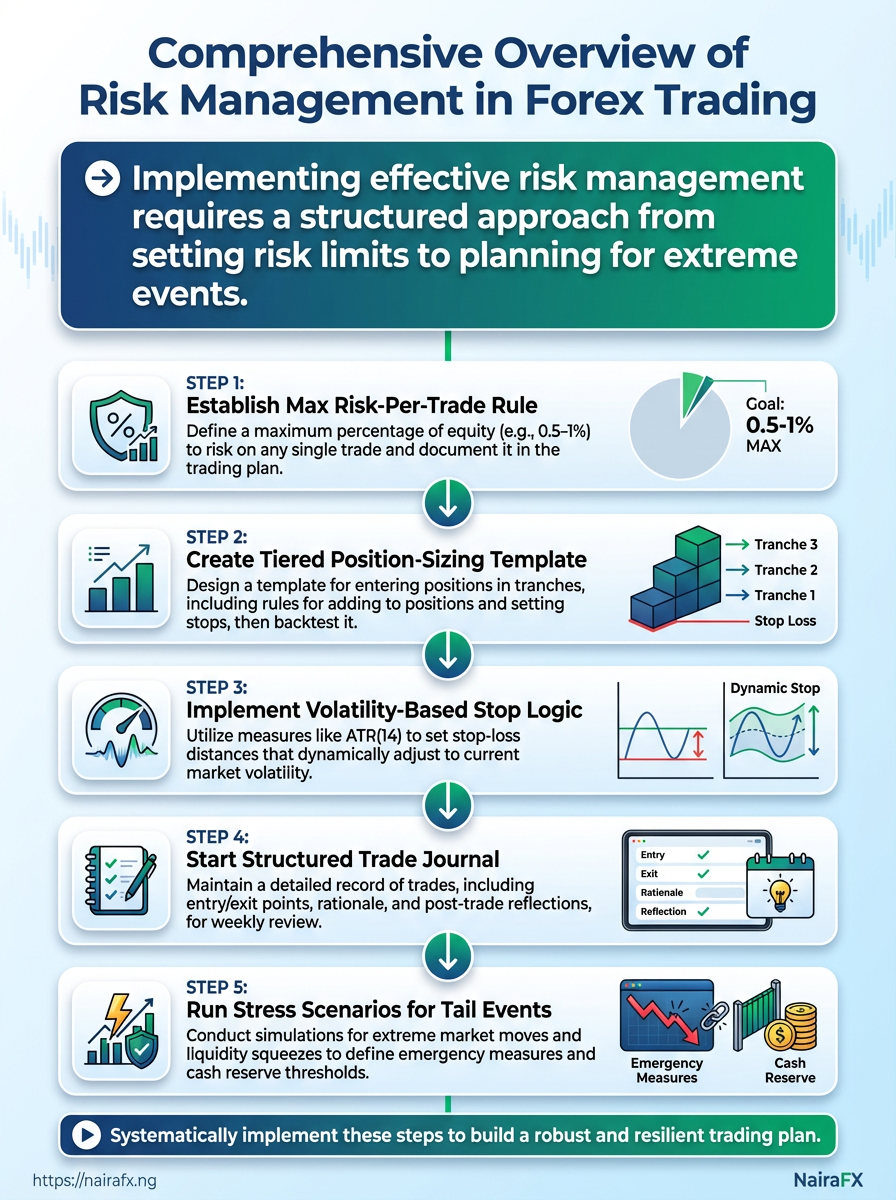

Trading in Nigeria’s volatile markets demands rules that survive stress, not just backtests. Start by capping exposure per trade, size positions in tiers rather than all at once, and use volatility-based stops so risk scales with market noise. Keep a disciplined trade journal and run scenario tests that include tail events and sudden liquidity squeezes. Those measures reduce ruin risk, keep drawdowns manageable, and make decisions repeatable under pressure.

Practical implications: Fixed risk cap: Limit each trade to a small percentage of equity so a string of losses can’t wipe the account. Tiered sizing: Add to winning positions in planned increments rather than compounding at random. Volatility stops: Use ATR(14) or similar measures to set stop distances that reflect current volatility rather than arbitrary pips. Trade journaling: Record entries, exits, rationale, and post-trade reflections to remove emotion from future decisions. * Tail-event planning: Hold cash buffers, test for extreme moves, and define rules for illiquid markets.

Recommended next steps (do these in order):

- Establish a

max risk-per-traderule (for example, 0.5–1% of equity) and write it into the trading plan. - Create a tiered position-sizing template with entry, add, and stop rules; backtest it on representative market periods.

- Implement volatility-based stop logic using

ATR(14)or a volatility percentile; simulate outcomes with a Monte Carlo tool. - Start a structured trade journal and review it weekly for rule adherence and behavioral patterns.

- Run stress scenarios for tail events and liquidity squeezes; define emergency measures (reduced position size, time-of-day exit rules, cash reserve thresholds).

Definition of common terms

Max risk-per-trade: The maximum percent of total equity risked on a single position.

Tiered position sizing: Entering a position in predefined tranches with specified stop and add rules.

Volatility-based stop: A stop distance calculated from current market volatility (e.g., ATR(14) multiples).

For traders who want to quantify these recommendations, Monte Carlo simulation and equity-curve evaluation bring huge clarity—services like the Monte Carlo and risk-management consulting available at NairaFX can turn these principles into tested rules. These steps are practical and actionable; implement them deliberately and the trading plan becomes something that performs in real markets, not just on paper.

Core Principles of Forex Risk Management

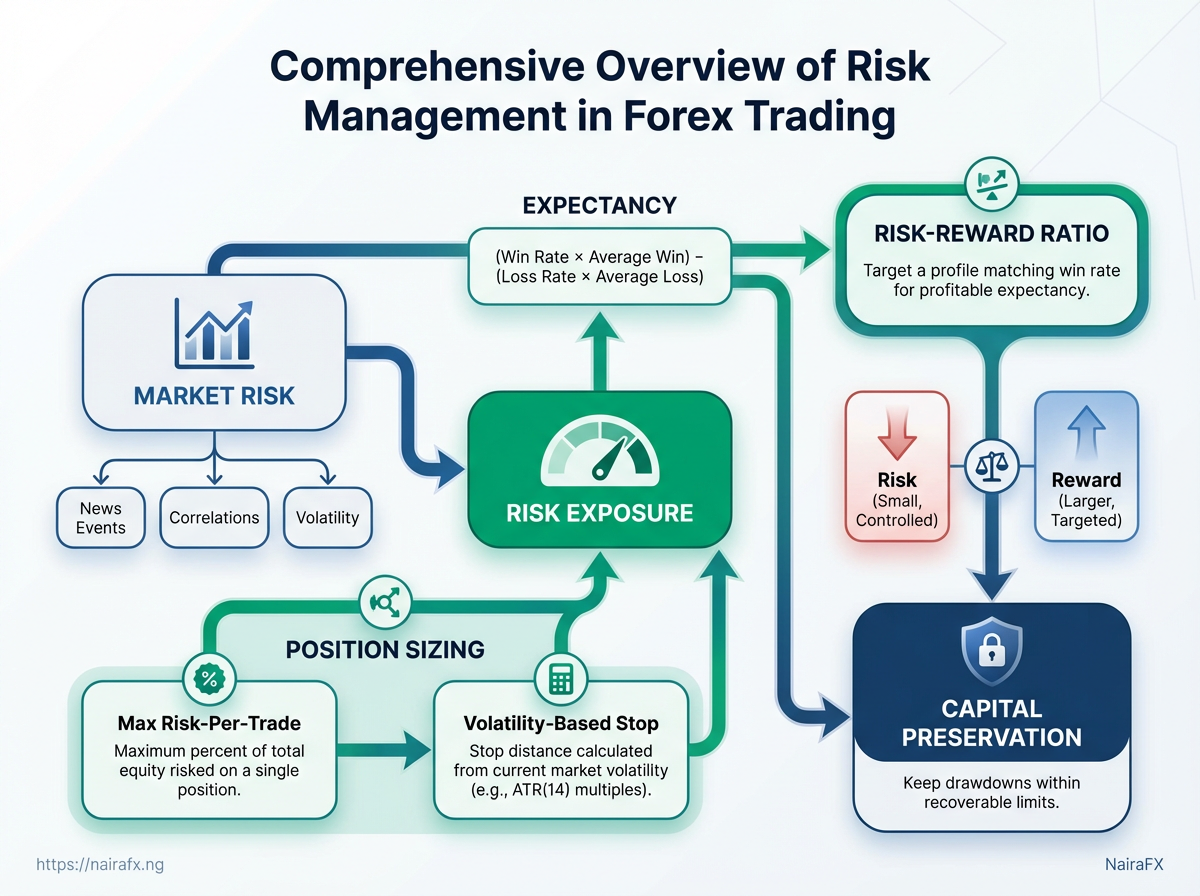

Capital protection sits at the top. Before thinking about edge or frequency, the trading plan must make sure losses can’t wipe out capacity to trade. That means setting a clear risk budget, keeping position sizes small relative to account equity, and treating expectancy and risk-reward as measurable properties of the system rather than vague hopes. Apply those rules consistently and emotional decision-making stops being the main driver of outcomes.

Capital Preservation: Keep drawdowns within recoverable limits by sizing positions so a streak of losses doesn’t bust the account.

Risk-Reward Ratio: Target a reward-per-risk profile that matches your win rate so that profitable expectancy is achievable.

Expectancy: expectancy = (win rate × average win) - (loss rate × average loss) — calculate this for each setup and strategy before trading it live.

Types of risk are straightforward but often underestimated.

Market Risk: Price moves beyond expectations, caused by news, correlations, or volatility spikes.

Liquidity Risk: Thin markets and wide spreads create slippage and execution problems, especially for large orders or at odd hours.

Counterparty Risk: Broker solvency, execution quality, and platform reliability affect the ability to close positions and withdraw funds.

Operational Risk: Connectivity failures, power loss, or misconfigured orders can turn a controlled trade into a disaster.

Practical rules to operationalize these principles:

- Set a daily/weekly risk budget: Max percent of equity at risk per day/week.

- Use position-sizing algorithms: Base size on

volatility-adjustedrisk, not fixed lots. - Predefine stop placement: Stops must reflect structure and liquidity, not emotion.

- Limit leverage: Match leverage to edge and drawdown tolerance.

- Diversify exposures: Avoid concentrated bets on one currency pair or macro theme.

- Decide your maximum account drawdown (e.g., 10%).

- Convert that to a per-trade risk limit (e.g., 0.5–1% of equity).

- Use volatility (ATR) to size positions to that risk.

- Backtest the approach and compute

expectancy. - Adjust leverage and stop rules until simulated drawdowns meet the budget.

Quick matrix showing which fundamental principles apply to different trading styles (scalping, day trading, swing, position)

| Principle | Scalping | Day Trading | Swing Trading | Position Trading |

|---|---|---|---|---|

| Capital Preservation | High — tiny sizes, frequent exits | High — controlled intraday risk | High — larger stops, manage overnight risk | Very High — largest absolute exposure, long-term drawdown control |

| Risk-Reward Ratio | Low–Mod — small R:R per trade, rely on win rate | Moderate — aim 1:1–1:2 | Moderate–High — 1:2+ common | High — 1:3+ desirable given low frequency |

| Win Rate vs Expectancy | Win rate critical — low R:R but high win % needed | Balanced — mix of rate and R:R | Expectancy-focused — fewer trades, higher R:R | Expectancy-critical — each trade must carry positive expectancy |

| Leverage Management | High sensitivity — tiny mistakes amplified | Moderate — intraday leverage ok with tight stops | Lower — use less leverage due to larger moves | Lowest — minimal leverage to protect capital |

| Diversification | Low — focus on a few liquid pairs | Moderate — multiple intraday setups | Moderate–High — spread across pairs/timeframes | High — diversify across themes and instruments |

Market practice shows matching the principle intensity to the trading style keeps risk measurable and manageable. Apply these rules consistently and the difference between guessing and deliberate trading becomes obvious.

Risk Measurement and Position Sizing

Start by deciding how much equity is genuinely at risk each time a trade is opened. Position sizing turns a trading idea into a controlled bet: it limits the capital exposed to any single move and keeps the overall portfolio within a pre-set loss tolerance. Practical sizing blends account equity, stop distance, instrument volatility, and portfolio correlations — not guesses.

Position sizing methods and worked examples

Fixed Fractional: Risk a constant percentage of equity per trade (e.g., 1%).

Fixed Dollar: Risk a fixed cash amount per trade (e.g., ₦50,000).

ATR-based (Volatility): Size positions so that stop distance ≈ k * ATR produces a consistent volatility risk.

Kelly Criterion: Uses edge and win-rate to compute an optimal fraction; usually scaled down for real trading.

Percent Equity: Similar to fixed fractional but applied at portfolio level for aggregated exposures.

Practical worked example — single currency pair

Account equity: ₦5,000,000 Risk per trade: 1% → ₦50,000 Entry: 1.5500, Stop: 1.5450 → Stop distance = 50 pips Currency pip value (per standard lot): assume $10 per pip; convert to Naira at current USD/NGN = ₦750 → pip value ≈ ₦7,500 per lot

position_size_lots = risk_per_trade / (stop_pips * pip_value)

So position_size_lots = ₦50,000 / (50 * ₦7,500) ≈ 0.133 lots (round to 0.13 lots).

When using volatility-based sizing, replace stop_pips with k * ATR (k often 1–2). Volatility sizing works better when markets shift regime; fixed fraction is simpler and robust when signals are noisy.

Portfolio-level risk: drawdown, correlation, stress tests

Value at Risk: Estimates probable loss over a time horizon at a confidence level.

Max Drawdown: Set a firm tolerance (for example, 10–20% depending on risk appetite) and stop adding risk when nearing that limit.

Correlation matrix: Build pairwise correlations across positions to detect concentration; a high correlation cluster means less effective diversification.

Stress testing steps:

- Define scenarios (e.g., USD/NGN 15% devaluation, global risk-off with 5% move in major FX pairs).

- Reprice positions under each scenario and calculate portfolio P&L.

- Compare scenario losses to max drawdown tolerance and liquidity constraints.

Practical tip: scale Kelly outputs by 25–50% to avoid oversized bets; combine ATR sizing with a fixed-fraction floor to prevent excessively large positions in low-volatility times.

Understanding per-trade risk and the portfolio’s behavior under shocks prevents unpleasant surprises and keeps trading decisions aligned with capital preservation. Keep sizing rules simple, measurable, and enforced — the discipline protects returns as much as the strategy itself.

Tools, Orders and Hedging Techniques

Start with order selection: choosing the right order type shapes execution quality and risk control more than most traders realise. Use market orders when speed matters and liquidity is deep; use limit orders to control price and reduce slippage. Combine functional order types—OCO, trailing stops and stop-losses—to automate exits and enforce discipline. Hedging moves risk off the directional book at a cost: effective hedges protect capital through asymmetric instruments like options when available, or via correlated instruments and position sizing when options markets are thin.

Order types and execution best practices

Order types and best-use cases for execution control

| Order Type | Use Case | Execution Risk | Typical Scenario |

|---|---|---|---|

| Market Order | Fast entry/exit in liquid markets | High slippage in low liquidity or during news | Entering large FX position in major pair during calm hours |

| Limit Order | Price control; add liquidity | Risk of missed fills if price doesn’t reach level | Scaling into position at a specific rate after pullback |

| Stop-Loss Order | Defined loss control | Can be triggered by spikes; slippage on gaps | Protecting capital overnight on equity positions |

| Trailing Stop | Lock profit while allowing run | Whipsaws in choppy markets | Riding trend on a breakout while preserving gains |

| OCO (One Cancels Other) | Manage alternative exit scenarios | Misplaced levels can leave both inactive | Placing take-profit and stop-loss simultaneously |

Key insight: Using defined orders reduces emotional errors and hidden execution costs; combine Limit for entries with OCO for exits to balance fill probability and risk control.

Execution tactics and practical steps

- Select time-of-day to trade.

- Avoid high-impact news windows; volume and spreads widen.

- Use

Limitwhen price discovery matters; useMarketto avoid missing fast moves. - Place stops beyond structural support/resistance, not round numbers.

Order sizing: scale into positions with smaller initial entries and planned pyramiding to reduce entry risk.

Hedging reduces directional exposure: Hedging reduces potential loss from adverse moves while incurring cost, such as option premia or financing on opposite positions.

Options hedge: Purchase puts/calls for asymmetric protection where options are liquid.

Correlation hedge: Short correlated instruments when options are unavailable; monitor basis and carry costs.

Hedge risk: Hedging can introduce basis, liquidity, and leverage risks; treat hedges like active positions requiring monitoring.

Practical example: buy a core long forex position, purchase a small put option for crash protection, and place a trailing stop to capture upside while limiting downside.

Use automation to enforce these rules but verify logic in a demo account first. This combination of disciplined order use and pragmatic hedging keeps capital protected without killing upside potential, especially in volatile Nigerian market conditions.

📝 Test Your Knowledge

Take this quick quiz to reinforce what you’ve learned.

Psychology, Operational Controls and Discipline

Traders lose more to their own heads than to markets. Emotional reactions—revenge trading after a loss, clinging to winners, or deviating from rules under boredom—create predictable leaks in performance. Practical routines and robust operational controls turn those leaks into manageable noise: a disciplined pre-trade checklist, a weekly review of a structured journal, and clear contingency rules for platform, connectivity, and capital stress.

Behavioral traps and trading routines

- Pre-trade criteria: Set objective entry, stop, and target rules before risking capital; if criteria aren’t met, no trade.

- Structured trade journal: Log entries consistently and review outcomes weekly to separate luck from skill.

- Cooling periods: After a loss that breaches a predefined drawdown threshold, take a time-based break (

30–120 minutes) to avoid emotionally-driven decisions. - Routine anchoring: Trade only during predetermined windows to reduce decision fatigue and sampling bias.

- Micro-goals: Use short, measurable objectives (e.g., “two quality setups today”) rather than P&L targets.

- Decide and write down pre-trade rules for size, risk-per-trade, and trade rationale.

- Record every trade immediately with objective fields (see table below).

- Schedule a weekly 45-minute review to tag recurring patterns and update rules.

- Implement a

loss-circuit-breaker: stop trading for the day after a set streak or percentage loss.

Operational controls and contingency planning

Operational resilience is as important as proper sizing. Plan for realistic failures and rehearse responses.

- Connectivity & platform failure: Maintain a backup internet (mobile hotspot) and a secondary trading device with platform credentials ready.

- Liquidity buffer: Keep a cash buffer for margin calls—enough to cover at least several days of worst-case volatility.

- Emergency exit rules: Predefine exits for extreme scenarios (sudden volatility, pairs halting) including market and limit-based fallbacks.

- Access & permissions: Keep recovery docs and 2FA methods accessible offline in secure storage.

Trade journal template fields and purpose for each field

| Field | Why it matters | Example entry | Review action |

|---|---|---|---|

| Date/Time | Contextualises session conditions | 2026-01-05 09:32 GMT+1 | Check time-of-day performance patterns |

| Currency Pair | Identifies instrument-specific edges | USD/NGN spot | Track pair-specific win rate |

| Position Size | Enforces risk limits | 0.5 lot / 1% risk | Verify adherence to risk rules |

| Entry/Exit Reason | Documents rationale vs emotion | Breakout after consolidation | Validate plan vs execution |

| Outcome and Lesson | Forces learning from result | +40 pips; held despite signal fade → exit earlier next time | Tag for rule update or confirmation bias |

The journal fields above make behavioral patterns visible and actionable; reviewing them weekly converts subjective feelings into objective rule changes.

A few practical warnings: rehearse emergency procedures so they become automatic, and make cooling periods non-negotiable. Discipline and simple operational redundancy reduce the number of decisions made under stress—and that reliably improves outcomes.

Regulatory, Market-Specific and Country Risks

Regulatory gaps, broker practices and country-level frictions create the riskiest blind spots for traders operating in Nigeria and similar emerging markets. Start by treating broker choice and settlement mechanics as operational risk — not just a cost of doing business. Brokers can be solvent on paper and still expose clients to slow withdrawals, poor FX execution, or legal uncertainty if their regulatory cover is weak or misaligned with where the client lives.

Negative Balance Protection: A broker policy that prevents client equity from falling below zero during volatile moves.

Client Fund Segregation: Practice of keeping client money separate from broker operating accounts to protect against broker insolvency.

Practical checks and examples: Verify licences: Confirm the regulator on the broker’s site and match it against the regulator’s register. UK/Europe licences carry different protections than offshore licences. Watch settlement flows: Know typical withdrawal timelines and FX routing — local rails often add 24–72 hours and additional checks. Expect verification: Nigerian payment rails require KYC/AML checks and sometimes additional ID steps for high-value transfers. Plan for conversion costs: Currency conversion fees and spread can erode returns; assume conversion when sizing positions in USD-denominated accounts.

- Check the broker’s regulatory registration and cross-reference the regulator’s public register (FCA, CySEC, SEC Nigeria).

- Confirm whether client funds are segregated and whether the broker offers negative balance protection.

- Test a small withdrawal and track timing, fees, and communication before scaling capital.

Checklist comparing broker attributes to verify (license, fees, segregation, negative balance protection)

| Attribute | What to check | Why it matters | Red flags |

|---|---|---|---|

| Regulatory License | Jurisdiction and registration number | Determines legal oversight and complaint avenues | License missing or offshore-only jurisdiction |

| Client Funds Segregation | Written policy; auditor statements | Protects client assets on broker insolvency | No segregation or mixed-account wording |

| Withdrawal Speed | Typical processing time and payout rails | Affects liquidity and ability to cut losses | Withdrawals >5 business days or opaque timelines |

| Negative Balance Protection | Policy scope and exceptions | Limits tail-risk exposure in flash events | No NBP or it’s conditional/limited |

| Operational Jurisdiction | Where company is incorporated and where services are offered | Affects enforceability and tax/regulatory compliance | Broker licensed elsewhere but markets Nigerians without local presence |

Key insight: Verifying these attributes prevents common operational losses: delayed exits, frozen funds, and surprise currency costs. Test the broker with small transfers and keep records of communication for disputes.

Industry-savvy traders also stress-test strategies against settlement lag and FX slippage — Monte Carlo simulation and equity-curve risk evaluation help quantify those effects. Treat regulatory and country risk like latency: measurable, testable and manageable with the right checks and small-scale experiments before committing meaningful capital.

Implementation Plan, Examples and Case Studies

Start by locking down the trading rules and position-sizing framework, then layer discipline tools (journaling, review cadence, stress tests). The plan below turns strategy concepts into operational steps traders can run in the first 90 days and then maintain.

Phased implementation checklist with tasks and success criteria for 30/60/90 day milestones

| Timeframe | Primary Task | Success Criteria | Owner/Responsibility |

|---|---|---|---|

| Day 1-30 | Establish rules and position-sizing; set up trading journal | Rules documented, position sizing rule applied to every trade, first 30 trades logged | Lead trader |

| Day 31-60 | Introduce weekly reviews, refine rules; start Monte Carlo stress tests | Weekly review notes show improvements, Monte Carlo run completed, max-drawdown estimate established | Trader + Risk analyst |

| Day 61-90 | Implement adjustments from tests; automate risk controls (alerts, stop placement) | Alerts active, automated stops tested in demo, 90-day equity curve evaluated vs baseline | Trader + Operations |

| Ongoing | Maintain journaling, monthly stress tests, quarterly strategy review | Monthly stress-test reports, journal kept, performance meets risk targets | Trader / Risk Manager |

Key insight: Use the first 30 days to hard-code discipline, the next 30 to stress and refine, and the final 30 to automate and operationalize those changes. That sequence converts behavioral rules into reliable systems.

Practical steps to execute this plan:

- Create a written trading plan and position-size formula, then apply it to every trade for 30 days.

- Pause weekly to review entries, exits, and rule adherence; flag recurring mistakes in the journal.

- Run Monte Carlo simulations on the realized equity curve to see realistic drawdown ranges.

- Implement automated alerts and stop rules in the trading platform; test in a demo for two weeks.

- Recalibrate expectancy and position-sizing based on 90-day results and stress-test output.

Short case studies and lessons learned

- Disciplined rules converted to consistent returns: A discretionary trader who enforced a

1% per-traderisk rule reduced position-sizing errors and cut max drawdown by roughly half over three months. - No rules → unstable equity curve: A trader without a documented plan chased winners and averaged larger losses; monthly volatility doubled versus peers.

- Stress-testing prevents surprises: Running simple Monte Carlo tests revealed a plausible 25% tail drawdown, prompting a conservative sizing tweak that preserved capital during a market swing.

Lesson One: Discipline beats clever tweaks — consistent application matters more than occasional brilliant calls.

Lesson Two: Journaling reveals repeatable mistakes — the fastest path to improvement is visible feedback.

Lesson Three: Stress tests change behavior — knowing worst-case ranges forces sensible sizing and grief-testing.

> “A simple rule followed consistently will outperform a brilliant rule followed sometimes.”

Turning rules into routines is where trading edges survive real markets — apply the checklist, keep honest records, and the probability of staying profitable rises substantially.

Quick Reference / Cheat Sheet

This is a compact, action-ready set of rules, formulas and checklists for everyday trading decisions — position sizing, stops, and the essential checks before and after a trade. Use the formulas for quick calculations and the checklists to avoid avoidable mistakes when markets move fast.

Compact formula table with parameters and example calculations

| Formula | Inputs | Example | Use Case |

|---|---|---|---|

| Risk amount = Account Equity × Risk % | Account Equity, Risk% | ₦100,000 × 1% = ₦1,000 |

Determine absolute currency risk per trade |

| Lot size = Risk amount / Stop distance (in account currency) | Risk amount, Stop distance | ₦1,000 / ₦200 = 5 micro-lots |

Turn risk allowance into trade size |

| ATR-based stop = ATR(14) × multiplier | ATR(14), multiplier (e.g., 1.5–3) | 0.0012 × 2 = 0.0024 (24 pips) |

Volatility-based stop placement |

| Kelly (simplified) = WinRate − (1 − WinRate) / RR | Win rate, Reward:Risk (RR) | 0.55 − (0.45 / 2) = 0.325 → 32.5% |

Theoretical optimal fraction (use conservatively) |

Key insight: These four compact formulas convert account-level risk decisions into concrete trade parameters quickly. ATR gives dynamic stops; Kelly suggests sizing but reduce it (e.g., use 1/4–1/2 Kelly) to stay conservative.

Top 10 risk management rules

- Limit risk per trade: Risk ≤ 1–2% of account equity.

- Use a stop always: Never trade without a predefined stop.

- Cap daily drawdown: Stop trading for the day after 3–5% loss.

- Size to volatility: Increase size when ATR is low, shrink when ATR rises.

- Avoid correlated exposures: Don’t run multiple trades that amplify the same risk.

- Define reward-to-risk: Prefer setups with RR ≥ 1.5:1.

- Scale out: Take partial profits to lock gains and reduce risk.

- Keep leverage conservative: Use no more than necessary to execute the plan.

- Recalculate after big wins/losses: Re-base position sizes to new equity.

- Record and review: Log every trade and review monthly.

Position sizing formulas (one-line)

- Risk amount:

Risk = Equity × Risk% - Lot size:

Lot = Risk / (PipValue × StopPips) - ATR stop:

StopPips = ATR(14) × Multiplier - Conservative Kelly:

Use Kelly × 0.25–0.5 for practical sizing

Pre-trade checklist

- Confirm trend and alignment across timeframes.

- Validate liquidity and economic calendar (no high-impact event).

- Calculate

Risk,Lot, andStop; ensure Risk ≤ plan. - Set entries, stops, and targets in the platform.

- Log entry/exit, rationale, and emotions.

- Measure outcome vs plan (win/loss, RR, slippage).

- Adjust rules if repeated deviations appear.

- Archive screenshot and update performance metrics.

Post-trade checklist

Keep this sheet accessible during trading hours — it reduces mistakes and keeps position sizing mechanical rather than emotional. The checks and formulas here translate strategy into disciplined actions that protect capital and compound returns.

📥 Download: Forex Trading Risk Management Checklist (PDF)

FAQ

Most traders succeed by keeping risk simple: choose a sensible percent of capital per trade, place stops where the trade idea breaks, and use hedging sparingly—only when it reduces portfolio drawdown without creating hidden correlations. Below are concise, practical answers to the common questions traders ask about these topics.

What risk-per-trade range is typical?

Industry practice usually sits between 0.5% and 2% of account equity per trade. Smaller accounts: aim for 0.5%–1% to protect capital and limit emotional stress. Established traders: 1%–2% can be appropriate if position sizing and edge are proven. * Reason to adjust: reduce the percent when volatility or uncertainty rises.

How should stops be placed?

Stops should reflect why the trade exists—place them where the thesis is invalidated. 1. Identify the reason for the trade (trend, breakout, mean reversion). 2. Locate logical technical levels (support/resistance, moving averages, structure). 3. Translate that level into price risk and size the position so the dollar risk equals the chosen percent.

Stop-placement approaches and logic Volatility-based stops: use ATR multiple to allow normal price noise. Structure-based stops: set beyond swing highs/lows or chart pattern boundaries. * Time-based stops: exit if the trade fails to progress within a planned timeframe.

When is hedging appropriate?

Hedging is useful when reducing specific, identifiable risk improves portfolio outcomes. Hedge for event risk: ahead of earnings, political events, or macro releases. Hedge to protect concentrated positions: when exiting is costly or taxes are an issue. * Avoid frequent directional hedging that doubles complexity and costs.

What common mistakes should be avoided? Over-sizing positions: emotional conviction doesn’t replace statistical edge. Moving stops outward to avoid losses: this destroys the validity of position sizing. * Hedging without measuring correlation: the hedge can increase net exposure unintentionally.

Practical tools such as position-size calculators, ATR filters, and Monte Carlo simulations help test these rules against realistic sequences of wins and losses. These trade rules keep decision-making clear and put downside management ahead of wishful thinking — the most reliable path to lasting returns.

Resource List

If building a practical toolkit for forex risk management, pick resources that pair immediate, actionable tools with deeper reference books and regulator pages for due diligence. Start with calculators and a trading journal you can use today, then layer in classic texts on position sizing and volatility-based stops. Use regulator sites to confirm broker credibility and local compliance — that step protects capital as much as any stop-loss rule.

Recommended quick tools and readings to keep at hand:

- Position sizing calculators: Use to translate risk percentage into lot size across account currencies.

- ATR-based stop calculators: Convert Average True Range into volatility-adjusted stops and targets.

- Trading journal templates: Track setups, edge frequency, psychological notes, and equity-curve metrics.

- Books on risk management: Deep dives on expectancy, Kelly, drawdown behaviour, and portfolio-level risk.

- Regulatory authority pages: Broker registration checks, complaints procedures, and leverage rules.

Organize resources by type (book, tool, regulator) with short descriptions and recommended use

| Resource | Type | Why it helps | Link/Where to find |

|---|---|---|---|

| “Risk Management and Financial Institutions” (John C. Hull) | Book | Comprehensive coverage of volatility, VaR concepts, and institutional risk frameworks | Major bookstores, academic publishers |

| Position sizing calculators (multiple) | Tool | Translate percent-risk into lot sizes; supports multiple base currencies and pip calculations | Broker educational pages, trading communities |

| ATR stop calculators | Tool | Converts ATR into stop distances for volatility-aware exits; useful for scaling and trailing stops | Trading tool websites and indicator repositories |

| Central bank / securities regulator pages | Regulator | Verify broker licenses, leverage rules, and local regulatory advisories | Nigeria: Central Bank of Nigeria & SEC Nigeria pages; other national regulator sites |

| Trading journal templates (Excel/Notion/Edgewonk) | Tool/Template | Record trades, setups, outcome categorization, and equity-curve analytics | Template marketplaces, journaling apps, community-shared spreadsheets |

Key insight: The right mix is one practical tool for daily use (position sizing/ATR calculator), one disciplined record-keeping habit (a journal), and one long-form reference (a risk-management book). Regulators anchor the stack by reducing counterparty risk.

A few practical tips: pick a position-sizer that handles your account currency, standardize journal fields before you trade, and use ATR stops only after testing them on historical sessions. Those small choices cut confusion and prevent preventable losses.

Conclusion

Trading through churn and sudden FX moves is more manageable when rules, sizing and routine replace impulse. Remember the practical fixes shown earlier: tighten position sizing after a run of losses, use stop placement tied to volatility rather than ego, and lean on simple hedges or limit orders when sovereign or liquidity risk spikes. A small set of disciplined controls—predefined risk per trade, realistic max-drawdown limits, and an operational checklist before market open—turns emotional reactions into repeatable behaviors. Examples in the article illustrated a trader who stopped a negative streak by switching from fixed-lot entries to volatility-adjusted sizing, and another who avoided a weekend gap loss by using a protective hedge and clear exit rules.

Next steps: start by updating your trade plan with one change (adjust risk per trade or add a daily stop), backtest that tweak for 30–60 trades, and document outcomes in a simple trade log. If implementation or platform setup is the bottleneck, resources like the NairaFX risk management guide explain setup examples and practical templates. For questions about prioritizing fixes or translating these ideas to your account size, treat the first two weeks as experiments—track one metric (win rate or average loss) and iterate. This approach keeps small mistakes small and makes steady progress more likely than chasing a perfect system.