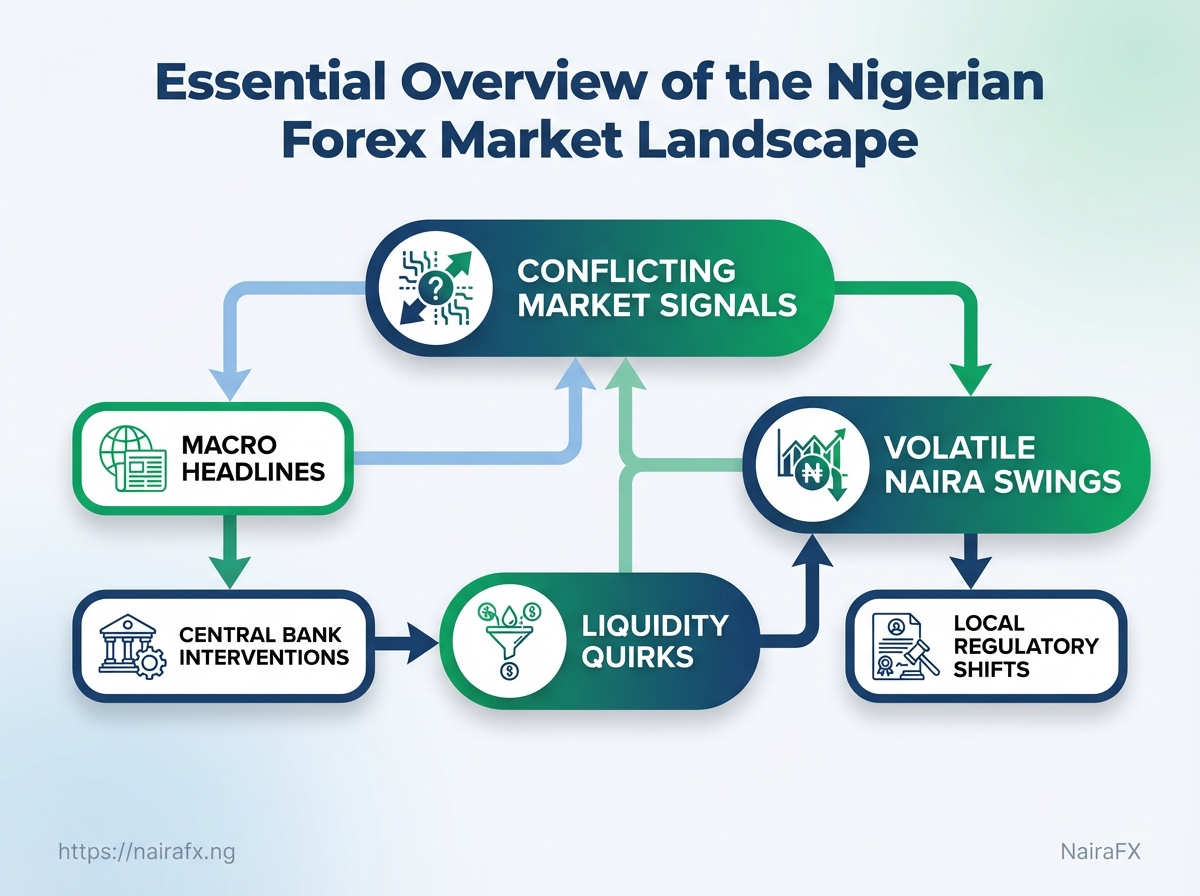

Most traders in Lagos wake up to two realities: volatile naira swings and an overload of conflicting market signals. The Nigerian forex market feels like a crowded trading floor where macro headlines, central bank interventions, and liquidity quirks collide every session. Knowing which signals matter and which are noise determines whether a position survives the day.

Local regulatory shifts, FX window fragmentation, and the growing overlap between onshore and offshore liquidity create opportunities — and sudden traps — for retail and institutional traders alike. Spotting the practical effects of policy moves on spreads, execution, and funding costs separates steady performance from emotional trading.

Market Structure and Key Players

The Nigerian FX market is a layered ecosystem where policy, commercial intermediation and offshore liquidity interact constantly. Price discovery doesn’t happen in a single venue — it’s the result of Central Bank actions, bank and bureau flows, broker execution and offshore providers supplying depth. Traders who understand who sets prices, who widens spreads in stress, and where liquidity sits will navigate volatility with much less guesswork.

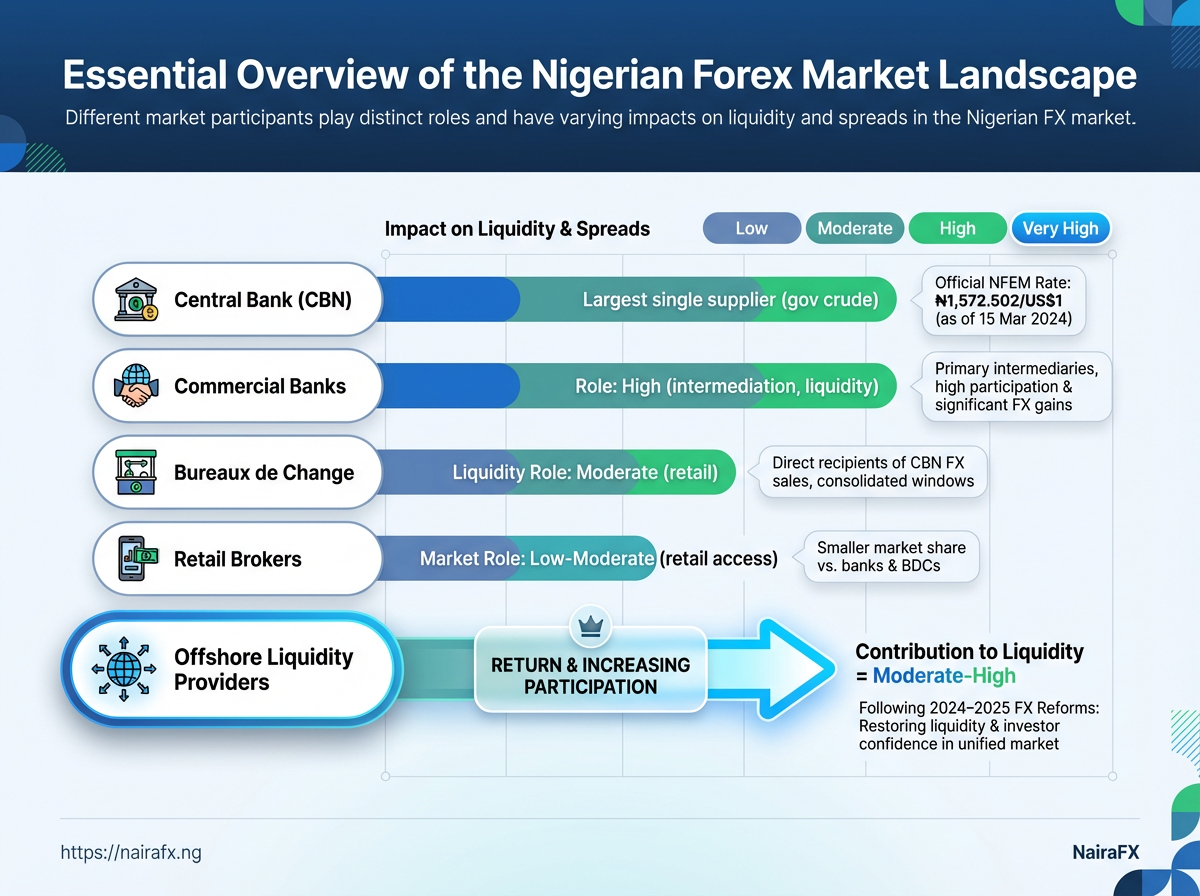

Central Bank (CBN): The CBN sets official rates through interventions, liquidity operations and policy guidance. Its actions determine onshore FX availability and often cause abrupt re-pricing when reserves, auctions or restrictions change.

Commercial Banks: These institutions provide most onshore liquidity for corporates and high-net-worth clients. They quote interbank-style prices for large trades but widen spreads for retail-sized fills and when their own net positions are stressed.

Bureaux de Change: BDCs supply retail cash and smaller wire FX, often at wider spreads and with limited depth. They’re crucial for physical cash needs and short-notice FX, but not for large electronic execution.

Retail Brokers: Online brokers give traders direct market access, differing by execution model (STP, ECN, dealer desk) and regulation. Execution speed, slippage and margin rules vary widely across platforms.

Offshore Liquidity Providers: Global banks and non-bank liquidity providers supply additional depth via offshore venues. They smooth large cross-border flows but can withdraw quickly during global risk-off episodes.

Market Participants and Their Roles

| Participant | Primary Function | Trader Impact (liquidity/spread) | Key Risk/Consideration |

|---|---|---|---|

| Central Bank (CBN) | Monetary policy, FX auctions, reserve management | High directional impact; sudden spread shifts when intervening | Policy opacity and intervention timing can create sharp moves |

| Commercial Banks | Onshore wholesale FX, corporate flows, hedging products | Primary liquidity source for large trades; spreads tighten for big volume | Credit limits, inventory risk, and internal hedging can restrict fills |

| Bureaux de Change | Retail cash exchange, small-value wire transfers | Immediate cash liquidity; wide spreads and limited depth | Susceptible to local cash shortages and regulatory checks |

| Retail Brokers | Market access, leveraged retail trading, order routing | Variable spreads; execution quality depends on model and partner LPs | Variable regulation and counterparty risk; watch slippage/margin calls |

| Offshore Liquidity Providers | Global interbank liquidity, pricing overlays, risk distribution | Deep pool for cross-border flows; can tighten pricing and reduce slippage | Access can be limited by capital controls and cross-border settlement frictions |

Key insight: The interaction between onshore policy actions and offshore depth determines how tight spreads stay during stress; retail traders should match execution venue to trade size and tolerance for slippage.

Practical rules: match trade size to venue, expect wider spreads during CBN operations, and treat bureau fills as tactical, not strategic, liquidity. Understanding these roles translates directly into better execution and more robust risk plans when markets move.

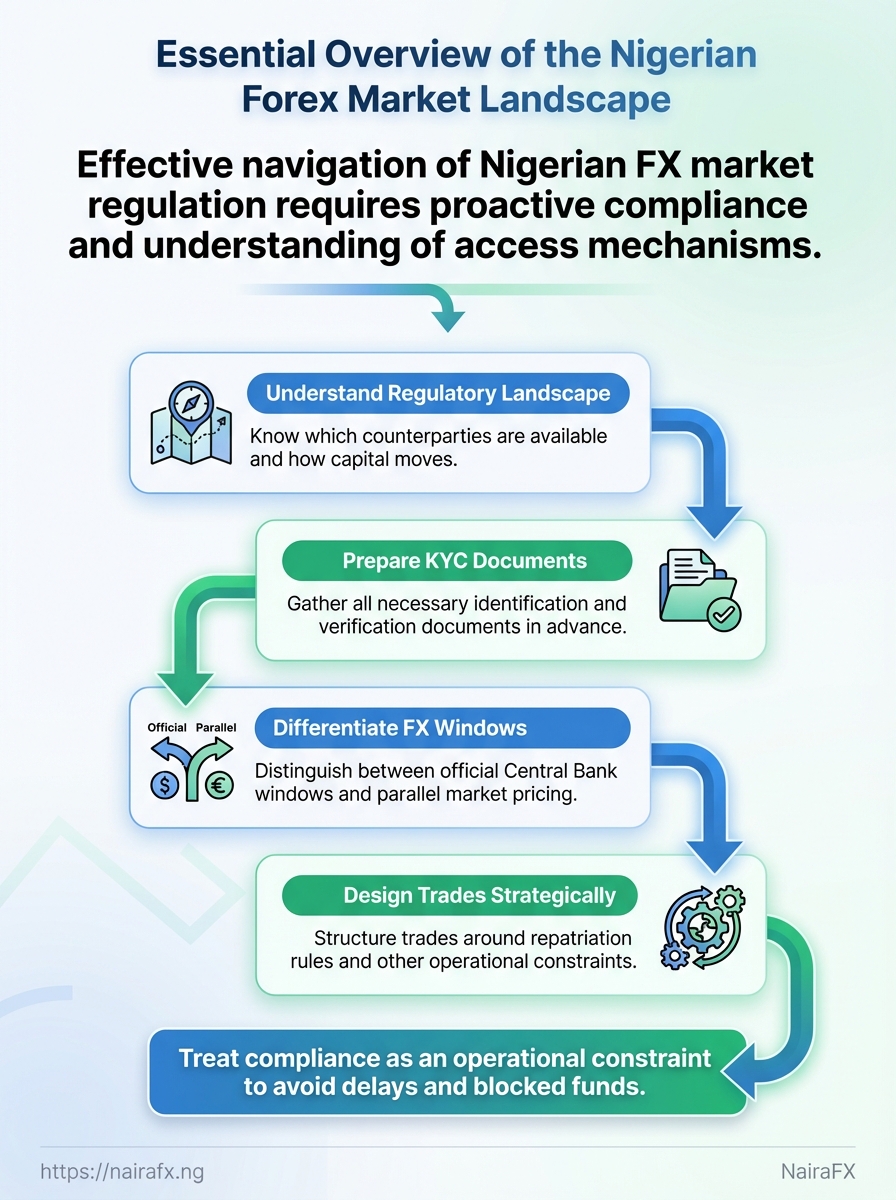

Regulation, Compliance, and Market Access

Regulation shapes what traders can actually do in Nigeria: which counterparties are available, how quickly capital moves, and what documentation gets you onboarded. Traders who treat compliance as an operational constraint — not an afterthought — avoid execution delays, unexpected costs, and blocked funds. Practical focus: know the difference between official Central Bank windows and parallel pricing, prepare KYC documents in advance, and design trades around repatriation rules.

Commercial Bank FX Desk: Banks typically execute client FX via CBN-approved windows, offering settlement in NGN with formal documentation; onboarding often requires comprehensive corporate/individual ID checks and can be slowed by liquidity limits. Licensed Retail Broker: Regulated brokers provide trading platforms and order execution; they enforce KYC and AML checks and may restrict leveraged products for local clients. Bureau de Change: Useful for small, retail cash needs; documentation is lighter but limits are stricter and pricing follows the parallel market. Offshore Broker (NGN access): Offers market access and product breadth; moving Naira on/offshore triggers repatriation controls and payment-provider scrutiny. Payment/Remittance Provider: Facilitates transfers between domestic and foreign accounts; subject to AML rules and CBN transfer limits that can delay settlement.

Practical checklist before opening any account: Prepare certified ID: passport or national ID, proof of address, and recent bank statements. Company docs ready: CAC records, board resolution, beneficial ownership if trading as a corporate entity. Understand pricing windows: official CBN rates vs parallel market differences. Plan for repatriation: confirm who bears FX conversion and approval steps. * Confirm limits and settlement times: daily trading caps, withdrawal lead times, and margin call procedures.

- Obtain and notarize

KYCdocuments. - Verify provider licensing and read onboarding SLA.

- Test small deposit/withdrawal to validate settlement path.

Practical Regulatory Considerations for Traders

| Provider Type | Required Documentation | Typical Onboarding Time | Constraints (e.g., repatriation, trading limits) |

|---|---|---|---|

| Commercial Bank FX Desk | Passport/NIN, bank statement, corporate docs (if applicable) | 3–10 business days | Subject to CBN windows; daily limits and liquidity constraints |

| Licensed Retail Broker | Passport/NIN, proof of address, bank reference | 1–7 business days | Leverage and product restrictions; NGN settlement paths vary |

| Bureau de Change | ID, recent utility bill | Same day–3 days | Small transaction caps; parallel market pricing |

| Offshore Broker (NGN access) | Passport, proof of funds, enhanced due diligence for large accounts | 5–15 business days | Repatriation approvals; potential local FX conversion fees |

| Payment/Remittance Provider | ID, proof of source of funds, beneficiary details | Same day–5 days | AML reviews can delay transfers; CBN transfer limits apply |

Key insight: onboarding speed trades off with regulatory scope — banks and offshore brokers require heavier documentation but offer deeper liquidity, while BDCs and remittance providers are faster but constrained by limits and parallel pricing. Confirm settlement paths before scaling positions.

Regulatory knowledge saves time and prevents capital from getting stuck mid-trade; treat compliance as part of strategy design rather than paperwork. If managing position size or running strategy simulations, model settlement delays and repatriation costs into expected returns.

Market Drivers: Macroeconomics, Oil, and Sentiment

Oil prices, central-bank balance sheets, and market mood jointly set the tempo for the naira. Movements in Brent change FX supply via government oil receipts; the Central Bank of Nigeria’s reserve swings reveal policy firepower; and inflation plus interest-rate differentials determine who wants to hold naira versus dollars. Traders who watch these three lenses together can anticipate directional pressure and position size, rather than reacting to headline noise.

Watchlist for active macro-driven trades:

- Brent sensitivity: Track crude moves and Nigerian fiscal breakevens for near-term FX supply shocks.

- Reserve signals: Large reserve drawdowns often precede tighter FX windows or import controls.

- Inflation vs. rates: Widening spreads between domestic inflation and policy rates erode real returns and pressure the currency.

- Portfolio flows: Equity and bond inflows/outflows shift Naira liquidity and short-term funding costs.

- Sentiment indicators: Local bond yields, Naira forwards, and FX swap rates show real-time risk appetite.

Oil revenues: Nigeria’s FX inflows are strongly correlated with the price of Brent and shipping/marketing timelines; fiscal lag can make the FX impact appear after price moves.

CBN foreign reserves: Reserve increases give the bank room to defend the naira; falling reserves often foreshadow tighter FX allocation or higher forward premia.

Inflation and interest-rate differential: When domestic inflation outpaces nominal policy rates, the real rate turns negative and foreign capital shrinks, weakening the currency.

Quick-reference matrix linking indicators to expected FX impacts and trader actions

| Indicator | Direction that Weakens NGN | Typical Timeframe of Impact | Trader Action |

|---|---|---|---|

| Brent Crude Price | Falling Brent reduces FX inflows and weakens NGN | Weeks to months (depends on export receipts) | Hedge with short USD/NGN, reduce long naira exposure |

| Foreign Reserves | Declining reserves signal reduced defense capacity and weaken NGN | Immediate to weeks | Lighten carry, increase FX liquidity buffers |

| Inflation (CPI) | Rising CPI (without rate response) erodes real yields, weakens NGN | Months | Avoid long naira carry; use inflation-linked hedges |

| Monetary Policy Rate (MPR) | Lowering MPR vs. global rates reduces carry appeal, weakens NGN |

Immediate to months | Reprice carry trades; prefer short-tenor positions |

| Net Foreign Portfolio Flows | Outflows reduce FX supply and weaken NGN | Days to weeks | Monitor flows; use stop-losses on long naira exposure |

Market data shows these indicators rarely move in isolation — a Brent shock plus reserve drawdowns and rising inflation creates a compound effect that amplifies currency moves. Traders who map expected timing (short vs. medium term) to position sizing and hedging instruments preserve capital and exploit clearer entry points. Keep these metrics on a dashboard and link them to position rules rather than gut feelings; that discipline separates reactive traders from consistently profitable ones.

📝 Test Your Knowledge

Take this quick quiz to reinforce what you’ve learned.

Market Instruments, Platforms and Execution

Immediate exposure often means trading the spot market; hedging constrained settlement needs pushes traders toward forwards or NDFs; short-term cash mismatches are best handled with swaps. Choose the instrument that matches the economic exposure, settlement constraints, and counterparty access rather than forcing a preferred product onto the problem.

Spot FX (NGN): Immediate exchange of currencies, usually T+2 settlement for major pairs; used for transactional flows and tactical currency bets.

Forward Contracts: Agreement to exchange at a future date at a fixed rate; used to lock in rates for known future cash flows or invoices.

Non-Deliverable Forwards (NDF): Cash-settled forward where onshore delivery is restricted; useful for hedging currency exposure when local settlement in the domestic currency is limited or regulated.

Currency Swaps: Exchange of principal and interest in different currencies over time; useful to manage funding mismatches and roll short-term FX exposure into longer tenor.

FX Options: Right, not obligation, to exchange at a strike; useful for asymmetric risk management or when preserving upside while limiting downside.

Practical execution and platform considerations

- Liquidity windows: Banks and ECNs concentrate liquidity during global trading hours; for NGN trades, liquidity is highest during Lagos/London overlap.

- Counterparty access: Retail platforms give spot access; institutional desk relationships or prime brokers needed for forwards, NDFs, and swaps.

- Settlement constraints: Onshore capital controls or FX windows dictate whether a deliverable forward is possible or whether an NDF is required.

- Cost components: Price comprises mid-market rate plus spreads, commission, and for forwards/swaps, implied financing costs.

- Operational risk: Confirm settlement instructions, nett positions, and MTM frequency; mis-specified instructions are a common source of failed trades.

Instruments by settlement method, use case, counterparty requirement, and liquidity profile

| Instrument | Settlement Type | Use Case | Liquidity / Typical Counterparty |

|---|---|---|---|

| Spot FX (NGN) | Deliverable (typically T+2) | Immediate cash needs, FX conversion for imports/exports | High intraday liquidity during market hours; banks, retail brokers |

| Forward Contracts | Deliverable at future date | Hedge known future payables/receivables | Moderate liquidity; bank counterparties and corporate FX desks |

| Non-Deliverable Forwards (NDF) | Cash-settled | Hedging where onshore settlement constrained | Liquidity concentrated in offshore markets; international banks, hedge funds |

| Currency Swaps | Exchange of principal/interest over time | Manage funding mismatches and tenor transformation | Lower liquidity than spot; large banks, corporates, institutional investors |

| FX Options | Exercisable right (cash or deliverable) | Asymmetric hedging, volatility trading | Varied liquidity; OTC with banks or on-exchange options where available |

Key insight: Matching settlement mechanics to the underlying exposure prevents basis risk and settlement failure; for Nigerian traders, NDFs and forward structures are common solutions when onshore NGN settlement is limited.

Execution choices shape costs and risks. Picking the right instrument for the exposure and using a platform with the right counterparty access reduces surprises and improves hedging effectiveness.

Risk Management, Position Sizing and Local Constraints

Practical risk controls start with realistic position sizing and explicit rules for execution when Nigerian market conditions break down. Use conservative position limits that reflect potential liquidity gaps, pair stop-loss placement with slippage planning, and keep access to multiple execution venues. These are not theoretical niceties — they change how quickly a losing trade becomes a manageable loss, or an illiquid market becomes a catastrophic one.

Position sizing and limits

Position sizing should be based on cash-at-risk rather than percent of account headline numbers. Calculate the maximum loss per trade in Naira, then translate that into lot sizes or contract sizes that respect likely slippage during off-peak hours. Rule-based sizing: Limit exposure to a fixed Naira amount per instrument. Volatility-adjusted sizing: Reduce size when implied volatility or realized ATR rises. * Concentration cap: No more than a set percent of portfolio value in any one currency pair or sector.

Order types and execution

Use stop-loss orders but assume slippage during thin liquidity windows. Favor limit entries for planned fills, market orders only for urgent exits, and bracket orders for automated risk enforcement. 1. Define acceptable slippage tolerance per instrument. 2. Use OCO (one-cancels-other) where supported to automate exits. 3. Keep a fax/phone fallback for brokers without reliable electronic fills.

Counterparty and access redundancy

Maintaining multi-provider access reduces execution risk if one broker’s pricing freezes or withdraws liquidity. Multi-broker access: Keep accounts with at least two brokers. Multi-venue routing: Use providers that can route across liquidity pools. * Operational checks: Weekly connectivity and fill-quality reviews.

Stress testing and scenario planning

Stress tests reveal where concentration and execution risk collide. Run worst-case scenarios (e.g., 5-sigma moves, local FX intervention) and Monte Carlo-style path simulations before increasing limits.

Definitions

Position Limits: Maximum exposure size per instrument expressed in Naira or lots.

Slippage Tolerance: Pre-defined acceptable deviation between requested and executed price.

Risk-control checklist matrix showing measure, purpose, implementation steps, and monitoring frequency

| Risk Control | Purpose | Implementation Steps | Monitoring Frequency |

|---|---|---|---|

| Position Limits | Prevent outsized exposure | Set max Naira loss per trade; convert to lots; enforce via order size checks | Daily |

| Counterparty Due Diligence | Reduce counterparty failure risk | Verify capital & regulatory status; review margin calls history; diversify brokers | Quarterly |

| Stop-Loss and Order Types | Automate loss control and manage slippage | Use stop-loss with slippage bands; prefer limit entries; implement OCO orders |

Trade-level / Daily review |

| Diversified Access (multiple brokers) | Avoid execution blackouts | Maintain 2+ brokers, test order routing, alternate funding methods | Weekly connectivity tests |

| Stress Testing & Scenario Planning | Identify tail vulnerabilities | Run historical shock scenarios; Monte Carlo of equity curve; plan margin buffers | Monthly / Before limit increases |

Key insight: The checklist shows simple, repeatable controls that translate directly into operational steps and monitoring cadence — the sort of discipline that prevents small losses from becoming institution-threatening events.

Applying these controls makes trading resilient to local quirks: smaller position sizes protect capital, redundant access preserves execution, and routine stress testing keeps surprises manageable.

📥 Download: Nigerian Forex Market Trading Checklist (PDF)

Practical Steps to Start Trading and Next Moves

Start trading by validating the simplest parts first: execution, funding flow, and basic risk controls. Run a lean 90-day program that proves the process end-to-end before increasing position sizes or automation. That early validation prevents costly scaling mistakes and makes performance problems visible when they’re still cheap to fix.

Trading account setup: Have a funded, verified account with the broker or counterparty you intend to use.

Connectivity check: Confirm API keys, MT4/MT5 or platform logins, and a reliable low-latency route.

Basic risk limits: Predefine daily max loss, per-trade size limits, and position concentration rules.

- Start small and validate funding flow.

- Track execution metrics continuously.

- Re-evaluate counterparties and collateral at milestones.

- Days 1–7: Onboard operationally and run controlled trades at minimum sizes.

- Days 8–30: Increase trade frequency, measure slippage, and collect latency histograms.

- Days 31–60: Introduce larger position sizes on proven signals and simulate stress scenarios.

- Days 61–90: Validate scaling rules, confirm collateral availability, and prepare escalation plans.

- Ongoing: Monitor execution metrics and re-assess counterparties quarterly.

What to monitor daily and why: Execution quality: Track slippage, fill rate, and time-to-execute. Operational health: Confirm settlement, margin calls, and funding confirmations. * Strategy drift: Compare realized P&L vs. expected outcomes and edge decay.

Step-by-step 90-day plan

90-day onboarding timeline with milestones, tasks, responsible party, and success criteria

| Day Range | Milestone | Key Tasks | Success Criteria |

|---|---|---|---|

| Days 1-7 | Operational onboarding | Set up accounts, API connectivity, run 10 dry-run orders |

All trades execute; funding flows verified |

| Days 8-30 | Execution validation | Run 100+ live micro-trades; record slippage, fill rate | Slippage within acceptable band; fill rate ≥ target |

| Days 31-60 | Scale testing | Increase ticket size; perform stress test; review margin | No unexpected margin calls; P&L aligns with projections |

| Days 61-90 | Counterparty & collateral review | Re-evaluate brokers, credit needs, settlement speed | Counterparty terms acceptable; collateral plan ready |

| Ongoing Monitoring | Continuous oversight | Daily execution logs; weekly performance reviews | Consistent execution metrics; documented anomalies |

Key insight: A structured 90-day timetable forces discipline—execution flaws surface early, counterparties and collateral needs become concrete, and scaling decisions are evidence-based rather than hopeful.

Slippage: Difference between expected and executed price; track per venue.

Fill rate: Percentage of orders filled at desired size; monitor by order type.

Time-to-execute: Measured latency from order submission to fill; log per instrument.

For traders operating in Nigeria’s volatile FX and equity environments, running this small-to-large validation prevents surprises from local liquidity quirks and settlement frictions. Including Monte Carlo scenario runs during Days 31–60 can highlight tail-risk behaviour before committing larger capital. Keep a close eye on execution metrics — they’re the clearest early warning system for operational or market problems.

Conclusion

After working through market structure, regulation, macro drivers and the nitty-gritty of position sizing, what matters is applying a few practical habits that survive volatility. Traders who anchored decisions to clear rules — a defined risk per trade, an execution plan tailored to local liquidity, and contingency hedges during oil-price swings — navigated past shocks with far less stress. Regulation and platform choice aren’t abstract hurdles; they shape access, slippage and counterparty risk in ways that quickly affect P&L. Remember the pattern: when macro signals diverge from sentiment, lean on rules and liquidity-aware sizing rather than gut calls.

Start with three actions you can do this week: – Set a hard risk limit per trade and document it. – Test execution on the platform you intend to use at low size to measure real slippage. – Build a simple hedge (or contingency plan) for extreme naira moves.

For professional resources and localized guidance, explore the practical guides at NairaFX, which detail platform choices and compliance steps relevant to Nigerian traders. If questions remain about sizing, hedge types, or how regulation affects your chosen instrument, return to the sections on risk and market access and apply the three actions above. Small, consistent changes to process beat sporadic guesses — the next profitable stretch starts with disciplined routines, not perfect forecasts.