You log into your trading platform after breakfast and find transfers delayed, a withdrawal flagged, or sudden KYC requests that make no sense — a familiar jolt for many active traders. Those shocks usually trace back to shifting forex regulations in Nigeria, where overlapping rules and changing enforcement can turn a routine trade into a compliance headache.

Understanding the practical shape of Nigerian trading laws matters less for theory and more for keeping capital mobile and avoiding unexpected penalties. Clear, sensible steps for compliance forex Nigeria reduce friction, protect margins, and stop regulatory surprises from eroding confidence and returns.

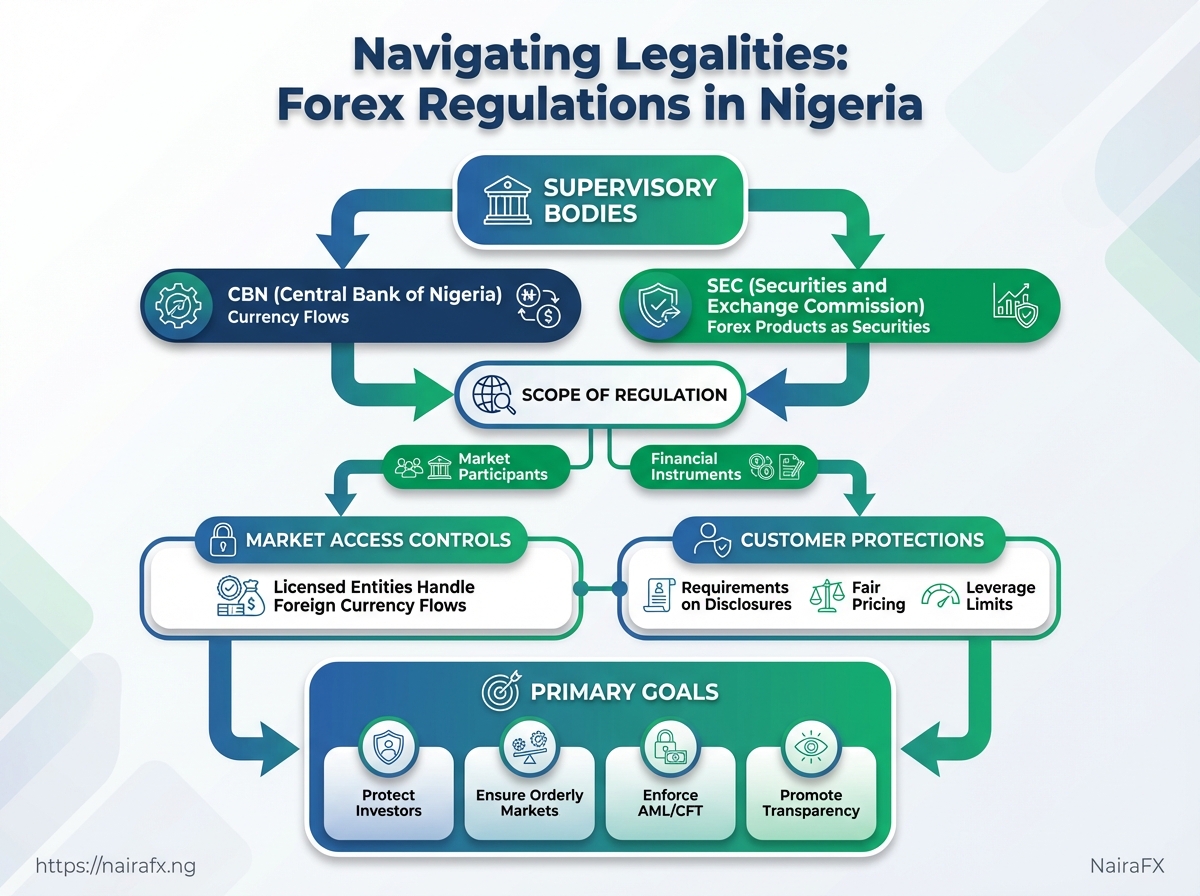

What Is Forex Regulation in Nigeria?

Forex regulation in Nigeria is the legal and supervisory framework that governs who can trade foreign exchange, which instruments are allowed, and how transactions are monitored to protect markets and participants. Regulators set rules to reduce fraud, prevent money laundering, ensure market integrity, and make sure retail traders aren’t exposed to unfair practices.

Regulation: The set of laws, rules, licenses, and supervisory actions that apply to forex dealers, brokers, banks, and payment service providers operating in Nigeria.

Scope of regulation: Which market participants and financial instruments the rules cover, including spot FX, forex derivatives, remittance services, and leveraged retail trading.

Primary goals: Protect retail investors, ensure orderly markets, enforce AML/CFT (anti-money laundering/counter‑terrorist financing) rules, and promote transparency across price discovery and settlement.

Supervisory bodies: The institutions responsible for creating and enforcing rules—most notably the Central Bank of Nigeria (CBN) for currency flows and the Securities and Exchange Commission (SEC) when forex products are packaged as securities.

What this looks like in practice:

- Market access controls: Licensed banks and authorised dealers must handle foreign currency flows for customers; unlicensed entities face penalties.

- Customer protections: Requirements on disclosures, fair pricing, and sometimes leverage limits for retail clients.

- Reporting and record-keeping: Banks and brokers must report suspicious transactions and keep records long enough to support investigations.

- Cross-border enforcement: Domestic regulators coordinate with foreign counterparts to investigate offshore brokers who solicit Nigerian clients.

How domestic rules interact with international brokers

- Offshore brokers that solicit Nigerian residents may still fall under Nigerian law if they target the local market.

- Regulators use licensing, warnings, and blacklists to deter non‑compliant foreign firms.

- Practical enforcement often relies on cooperation with foreign regulators and financial institutions for asset freezes and information sharing.

A trader should watch for licensing status, clear client fund segregation, and published AML/CFT procedures when choosing a broker. Knowing which rules apply reduces legal surprises and keeps capital safer in fast-moving markets.

How Does Forex Regulation Work in Nigeria?

Forex activity in Nigeria is governed through a mix of licensing, ongoing supervision, and enforcement actions that together try to protect market integrity and retail traders. Licensing determines who may operate (brokers, remittance service providers, authorized dealers), routine supervision keeps those firms within rules, and enforcement escalates when breaches threaten customers or the wider financial system. Traders benefit because regulation sets minimum standards for capital, reporting and client protections — and they suffer when enforcement is weak or unclear.

Who must be licensed and by which authorities

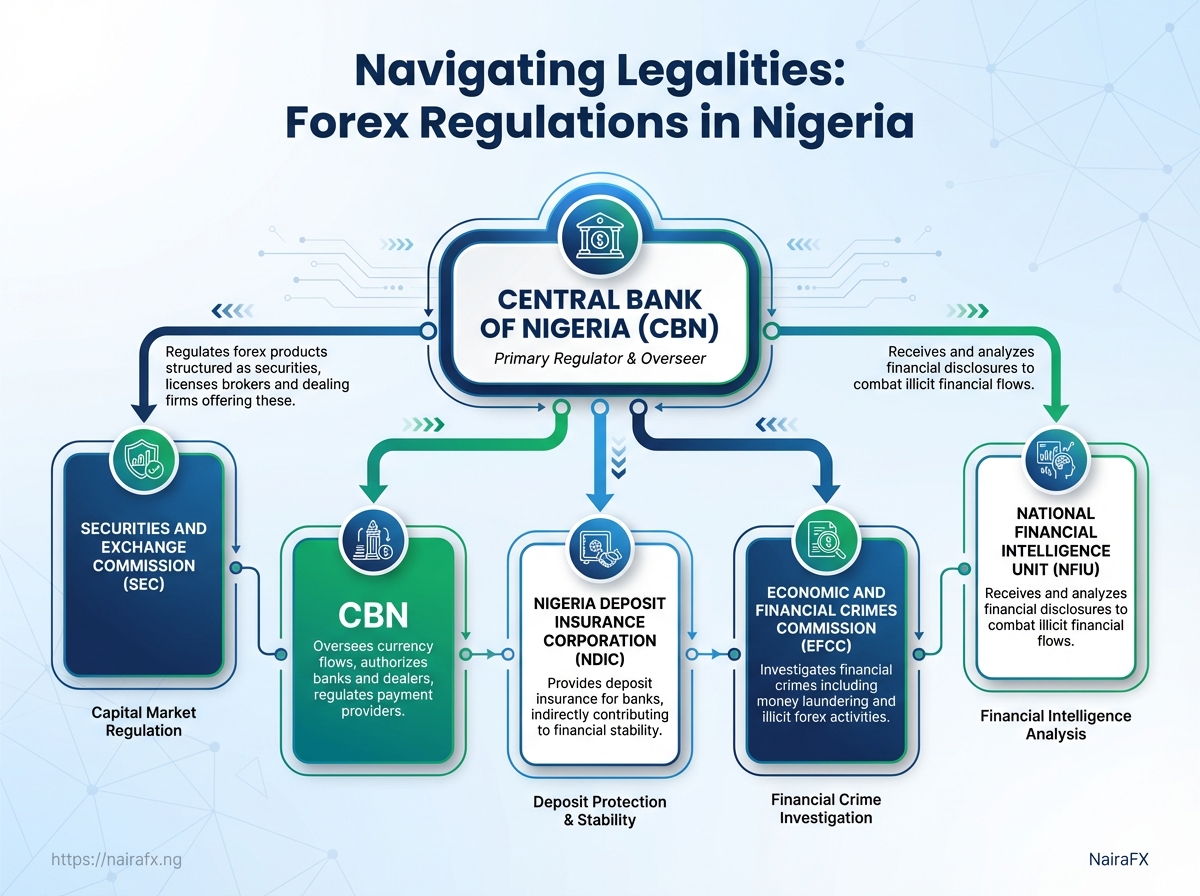

Brokers and dealing firms: Must be licensed by the Securities and Exchange Commission (SEC) when offering forex products that qualify as securities, or operate under CBN authorization when acting as authorized dealers in foreign exchange.

Banks and authorized dealers: The Central Bank of Nigeria (CBN) grants licenses to banks and non-bank financial institutions to deal in FX and oversees their foreign exchange operations.

Payment and remittance providers: Must register with the CBN and comply with Anti‑Money Laundering rules; those offering investment-like FX products may also fall under SEC oversight.

Compliance and risk officers within firms: Required roles, with firms expected to demonstrate internal controls and reporting lines.

How supervision differs from enforcement

- Routine supervision: Regular reporting, on-site inspections, audits, and compliance reviews that verify capital adequacy, client segregation, record-keeping and

KYC/AMLprocesses. - Escalation and enforcement: Triggered by serious breaches — market manipulation, fraud, lateral noncompliance. Enforcement can mean fines, licence suspension or revocation, criminal referral, and public sanctions.

Typical licensing process (step-by-step)

- Submit application and statutory documents to the relevant regulator with proof of capital and governance structures.

- Undergo background checks, fit-and-proper assessments, and technical reviews of systems and compliance policies.

- Receive conditional authorization pending operational checks, then full licence after demonstration of readiness.

Consequences for non-compliance that affect traders

- Operational interruption: Licence suspension halts trading access, freezing client positions or withdrawals temporarily.

- Loss of client protections: Firms forced into liquidation may leave clients unsecured without clear segregation of assets.

- Reputational contagion: Enforcement actions erode market confidence and can widen spreads or reduce liquidity.

Roles and powers of the main Nigerian regulatory bodies relevant to forex (what each regulates, typical actions they take, and whom they oversee)

| Regulatory Body | Primary Role | Powers/Actions | Who Is Covered |

|---|---|---|---|

| Central Bank of Nigeria (CBN) | Monetary policy & FX market supervision | Issue FX licences, set FX rules, impose sanctions, regulate authorised dealers | Banks, authorised FX dealers, payment service providers |

| Securities and Exchange Commission (SEC Nigeria) | Regulates capital markets and investment products | Licence securities brokers, enforce market conduct rules, issue fines/suspensions | Brokers, asset managers, firms offering FX as securities |

| Economic and Financial Crimes Commission (EFCC) | Investigates financial crimes | Criminal investigations, prosecutions for fraud, money laundering | Any entity/person involved in financial crimes |

| National Insurance Commission (NAICOM) | Regulates insurance sector | Licence insurers, supervise conduct, sanctions for breaches | Insurance companies (relevant when FX products tie to insurance) |

| Nigeria Deposit Insurance Corporation (NDIC) | Deposit protection and bank failure resolution | Provide deposit insurance, support bank resolution, protect depositors | Deposit-taking banks (indirect trader protection) |

Regulation matters because it shapes which firms are allowed to operate, what protections traders can expect, and how quickly problems get resolved. Understanding which regulator covers a provider is the most practical first step before placing funds.

Key Laws, Rules and Guidance Affecting Forex Trading

Foreign-exchange activity in Nigeria sits at the intersection of central-bank controls, anti-money-laundering obligations and securities/derivatives rules. Traders need to navigate a web of CBN circulars that control permissible FX flows, AML/CFT rules that shape onboarding and payment mechanics, and securities law where derivatives or CFDs are involved. Understanding which instrument applies in a given trade — and how it affects verification, settlement and reporting — reduces surprise compliance costs and operational drag.

Core regulatory touchpoints and practical effects:

- CBN FX controls: dictate who can access Naira or FX, allowable instruments for settlement and documentation required for transfers.

- AML/CFT requirements: force robust client verification, transaction monitoring and suspicious-activity reporting — this changes how brokers accept deposits, onboard clients and process withdrawals.

- Securities/derivatives rules: determine whether a product needs broker licensing, prospectus/registration or investor protections — CFDs and leveraged products can trigger SEC oversight.

- Tax rules: affect recordkeeping and whether trading gains are reportable as personal income, business profit or capital gain, changing how traders plan withdrawals and record trades.

- Cross-border payment circulars: influence how remittances and international transfers are routed, often requiring additional documentation and use of authorised dealers.

CBN circulars: These are the practical rules traders encounter daily; they arrive as circulars or guidelines rather than single statutes.

AML/CFT (Money Laundering (Prohibition) Act 2022): Lays out customer due diligence, reporting thresholds and penalties affecting KYC and transaction limits.

SEC regulations on derivatives and broker licensing: Apply when a product falls inside the securities/derivatives definition and when an intermediary offers leveraged products to Nigerians.

Tax rules (Finance Acts and tax codes): Determine tax treatment and required filing; traders must keep trade-level records for audit.

Cross-border payments guidance: Controls on outward remittances and FX settlement pathways that materially affect how international brokers pay out to Nigerian accounts.

Provide a structured list of laws and guidance: name, issuing body, year, and short trader impact summary

| Law/Guideline | Issuing Body | Year/Effective Date | Trader Impact (1-line) |

|---|---|---|---|

| CBN Foreign Exchange Guidelines (various circulars) | Central Bank of Nigeria (CBN) | Various (ongoing updates since 2015) | Restricts permissible FX flows, documentation for settlements and authorised dealer requirements |

| Money Laundering (Prohibition) Act | National Assembly / Federal Government | 2022 | Requires enhanced KYC, transaction monitoring and suspicious activity reporting for brokers and traders |

| SEC Rules on Derivatives & Broker Licensing | Securities and Exchange Commission (SEC) Nigeria | Regulatory framework evolving (SEC rules applied since 2010s; ongoing updates) | Triggers licensing, disclosure and investor-protection obligations for derivatives/CFD offerings |

| Tax Regulations & Finance Acts (income/capital gains rules) | Federal Inland Revenue Service / Ministry of Finance | Various (notable Finance Acts 2019–2020; ongoing) | Affects tax treatment of trading gains and recordkeeping for audit and filing |

| CBN Circulars on Cross-Border Payments | Central Bank of Nigeria (CBN) | Various (notable circulars 2016–2021) | Dictates documentation, permissible channels and timing for cross-border remittances and FX settlements |

Who Enforces Forex Rules — Regulatory Bodies & Their Roles

Nigerian enforcement is spread across a few authorities, each with a distinct remit. Knowing which body to approach for fraud, licensing, or AML concerns saves time and increases the chance of a useful response. Many retail forex providers operate offshore, which limits what local agencies can do — but there are clear routes for complaints and escalation when Nigerian law or consumer protection is involved.

Securities and Exchange Commission (SEC): The SEC oversees capital market operators and derivatives activities that fall inside Nigeria’s securities framework. Complaints about firms claiming to offer regulated securities, unlicensed investment schemes, or misleading investment products that target Nigerians are usually routed here.

Central Bank of Nigeria (CBN): The CBN regulates banks, payment service providers, and foreign exchange policy. Issues involving banks acting as payment gateways for fraudulent brokers, illegal currency transfers, or violations of FX rules often warrant contacting the CBN.

Economic and Financial Crimes Commission (EFCC): The EFCC handles financial crime investigations, including large-scale fraud, money laundering, and advance-fee schemes that affect the public. Escalate clear cases of fraudulent trading platforms or organized scams to the EFCC.

Nigeria Financial Intelligence Unit (NFIU): The NFIU collects and analyses suspicious financial transaction reports. If AML breaches are suspected — unusual deposit/withdrawal patterns or structuring to avoid reporting — the NFIU is relevant (often working with EFCC/CBN).

Consumer Protection / State Agencies: State-level consumer protection agencies and the Federal Competition and Consumer Protection Commission can help with unfair business practices, false advertising, and refund disputes when other regulators don’t apply.

Practical steps to escalate a complaint

- Gather documentation: trade confirmations, account opening emails, deposit receipts, screenshots of chats, and any promotional material.

- Contact the broker: lodge a formal complaint via their official channel and save timestamps and reference numbers.

- Escalate to your bank/payment provider: file a chargeback dispute or request transaction reversal if payments were recent.

- File with regulators: send concise complaint packets to the SEC, CBN, or EFCC depending on the issue, attaching evidence and the broker’s responses.

- Use public reporting: report on consumer forums and currency trader communities to warn others while you pursue formal channels.

Limitations when dealing with offshore brokers

- Jurisdiction gap: Offshore registration often places the broker outside Nigerian reach, limiting enforcement power.

- Enforcement cost: Cross-border legal action is expensive and slow; authorities may prioritize systemic risks.

- Recovery uncertainty: Even when authorities act, recovering funds can be difficult without international cooperation.

Practical tools to include: a complaint checklist, screenshots of required documents, and template wording for regulator complaints. Knowing which agency to approach and having evidence organised makes escalation faster and more effective—exactly what matters when funds and reputation are at stake.

Compliance Checklist for Traders and Brokers

Start by treating compliance as an operational habit, not an occasional task. Traders and brokers who build simple, repeatable verification routines avoid most disputes and sudden headaches. Below are practical actions, specific documents to keep, red flags to watch for, and a short step-by-step verification process you can run before committing funds.

KYC: Know-your-customer procedures that verify identity and reduce fraud risk.

AML: Anti-money-laundering controls that monitor suspicious flows and reporting obligations.

Practical checks every trader should do:

- Confirm registration: Verify broker registration with the relevant regulator.

- Check disclosures: Ensure leverage, fees, and margin calls are clearly published.

- Document retention: Keep copies of

ID,proof of address, and trade confirmations. - Withdrawal test: Make a small deposit-and-withdrawal to validate processing times.

- Customer support: Confirm live, documented dispute resolution channels exist.

- Visit the regulator’s public registry and search the broker name.

- Compare the broker’s legal entity name with platform branding and

terms & conditions.

- Request KYC requirements up front and keep all submitted documents with timestamps.

How to spot red flags: unlicensed claims, promises of guaranteed returns, hidden withdrawal conditions, or refusal to provide clear legal entity details. If a broker dodges simple questions about regulation or uses pressure tactics (e.g., “deposit now or miss the opportunity”), treat that as a material risk and pause.

Checklist matrix: compliance item, how to verify it, expected document or proof, action if non-compliant

| Compliance Item | How to Verify | Expected Proof/Document | Action if Non-compliant |

|---|---|---|---|

| Broker registration status | Check regulator registry and cross-check legal entity name on site | Screenshot of registry entry, regulator reference number | Do not fund; report to regulator and seek alternative broker |

| KYC/AML checks | Ask for KYC list and sample onboarding flow | Copies of ID, proof of address, onboarding timestamps |

Stop onboarding; escalate to compliance team or regulator |

| Deposit/withdrawal transparency | Review T&Cs, test small deposit/withdrawal | Transaction receipts, withdrawal timeline screenshots | Freeze additional deposits; file formal complaint |

| Leverage and instrument disclosure | Read product disclosure statements and margin manuals | PDS or product brochure, margin call policy pdf | Refuse trades using undisclosed leverage; seek refund if mis-sold |

| Customer support & dispute resolution process | Contact support, request escalation path and SLAs | Support tickets, email confirmations, dispute policy page | Open formal dispute; use regulator mediation if unresolved |

Common Misconceptions and Legal Myths

Many Nigerian traders assume forex is either a legal grey area or that rules don’t apply the same way as for local stocks. That’s not true. Forex trading is regulated by Nigerian authorities when it involves local banks, naira flows, or Nigerian-resident brokers, and international platforms still create legal and tax obligations for Nigerian residents. Treating forex as risk-free because it happens “overseas” is a dangerous misconception.

Myths and realities for Nigerian forex traders

- Myth — Offshore accounts are magically untouchable.

- Myth — Forex profits aren’t taxable if reinvested.

- Myth — Regulators don’t enforce forex rules in practice.

Tax obligations and enforcement likelihood

- Register tax status and track trades.

- Report realized gains as part of personal or corporate income returns.

- Keep clear records: account statements, trade logs, and bank transfers.

Industry analysis shows tax authorities focus on large flows and persistent mismatches between declared income and bank activity. Smaller retail traders may not face immediate audits, but regular profitable traders should treat tax compliance as a business necessity.

Persistent misconceptions about offshore protections

- Belief that KYC/AML are optional overseas. Banks and brokers keep records and may share them under legal requests; KYC/AML rules are widely implemented.

- Assumption that currency conversion happens without friction. Converting profits to naira can incur delays, spread costs, and require documentation; plan liquidity accordingly.

- Thinking platform T&Cs don’t matter. Terms govern dispute resolution, withdrawal limits, and legal recourse—read them.

Record-keeping: Maintain trade logs, timestamped account statements, and proof of transfers.

Compliance posture: If trading at scale, model taxes and drawdown scenarios — tools like Monte Carlo simulation can reveal how taxation and withdrawal timing affect strategy viability.

Treat legal clarity and tax compliance as part of risk management, not afterthoughts. That approach keeps strategies viable and avoids costly surprises down the road.

Real-World Examples & Case Studies

Practical incidents stay with traders longer than theory—these three condensed case studies show how governance, paperwork and simple pre-trade checks prevent losses and save weeks of dispute handling.

Offshore broker withdrawal refusal An individual client deposited via an offshore platform and later requested a withdrawal after profits. The broker cited ambiguous T&Cs and a “risk-review.” The trader escalated to the platform’s compliance desk, then to the regulator in the broker’s jurisdiction. Resolution required proof of source-of-funds, trade logs, and multiple correspondence timestamps. Lesson: Document everything: save deposits, trade confirmations, and chat transcripts immediately after each interaction.

Account freeze due to AML red flags A corporate client received an urgent account freeze after several high-value incoming transfers from third-party accounts. The broker’s AML unit flagged unusual counterparty patterns and froze withdrawals pending verification. The client supplied notarized invoices, bank-letter confirmations and a compliance remediation statement; funds were released after 12 business days. Lesson: Proactive paperwork reduces downtime: have beneficial_owner details, invoices and bank correspondences ready before large moves.

Pre-trade compliance that saved a margin event A mid-sized prop firm tested a new high-leverage strategy. Pre-trade margin simulation and a quick Monte Carlo run revealed a 1-in-20 chance of margin call under stressed FX moves. The desk reduced leverage and added a dynamic stop-loss; the next volatile session would have otherwise triggered a costly close-out. Lesson: Simulate before you scale: small computational checks can prevent catastrophic tail losses.

Chronological summary of each case study: date, parties, trigger event, regulatory action, outcome and lesson

| Case | Trigger Event | Regulatory Action | Outcome | Lesson |

|---|---|---|---|---|

| Offshore broker withdrawal refusal | Withdrawal dispute after profitable exit | Broker review; escalation to offshore regulator | Withdrawal released after KYC & timeline proofs | Keep transaction and chat records; escalate early |

| Account freeze over suspicious transfers | Multiple third-party incoming transfers | AML freeze; paperwork request | Funds released in ~12 business days after verification | Pre-package compliance docs for corporate moves |

| Local broker insolvency and client funds | Broker liquidity stress leading to suspension | Local regulator placed broker under supervision | Clients entered claims process; partial recoveries | Split custody and limit exposure to single broker |

| Successful dispute resolution via regulator | Contractual ambiguity on margin closeouts | Regulator mediated; required trade logs | Trader regained partial losses via settlement | Open formal complaints faster; follow regulator templates |

Keeping these patterns in mind makes compliance work less like paperwork and more like preventive medicine—small, habitual actions that stop big problems before they start.

How Traders Can Stay Compliant — Practical Next Steps

Start by treating compliance like part of your trading edge: clear records, consistent checks, and a plan for escalation turn regulatory risk into manageable overhead. New or uncertain traders should follow a short, repeatable workflow that protects capital, reputation, and access to platforms.

- Assess your status and obligations.

KYC and AML in your jurisdiction.

- Register where required.

- Set up standard record-keeping.

- Implement formal

KYCandAMLchecks.

- Run risk and compliance reviews regularly.

- Create an escalation framework.

- Maintain ongoing education.

Templates and record-keeping best practices

Trade Log: Date, instrument, entry/exit price, size, P&L, rationale, screenshots.

Funding Ledger: Source of funds, amount, date, wallet/account ID, supporting docs.

Correspondence Archive: Broker emails, agreement PDFs, dispute records, dated and indexed.

Best practices include:

- Consistent naming: use YYYYMMDD prefixes for files.

- Immutable snapshots: save screenshots and signed agreements.

- Encrypted backups: store offsite encrypted copies.

When to escalate

Internal escalation: Significant unauthorized trades, repeated platform errors, or unexplained balance changes. Legal counsel: Contract disputes, potential breaches of Nigerian trading laws, or complex cross-border taxation questions. Regulator notification: Clear evidence of fraud, market manipulation, or when laws explicitly require reporting.

Industry analysis shows that disciplined record-keeping and clear escalation rules prevent small compliance lapses from becoming business-ending problems. Use straightforward systems now and they’ll save time and risk later.

Conclusion

After the jolt of a flagged withdrawal or an unexpected KYC request, the sensible path is simple: understand the rules, document your trades, and keep communication lines open with your broker and regulator. The article showed how Nigeria’s regulatory framework assigns roles (CBN, SEC) and how common issues — delayed transfers, account freezes, sudden compliance checks — typically trace back to KYC gaps or mismatched paperwork. Keep records, update KYC proactively, and choose brokers with clear compliance procedures to avoid most disruptions.

If wondering what to do next: 1) run a quick compliance audit of your account details, 2) keep copies of deposit/withdrawal receipts and ID documents, and 3) contact your broker immediately when a hold appears while escalating to the regulator only if unresolved. Traders who followed the case studies here resolved freezes faster by providing transaction trails and proof of source of funds. For a practical checklist and local guidance, see the NairaFX compliance resources. Those steps reduce surprise downtime and make navigating Nigerian trading laws and forex regulations in Nigeria far less stressful.