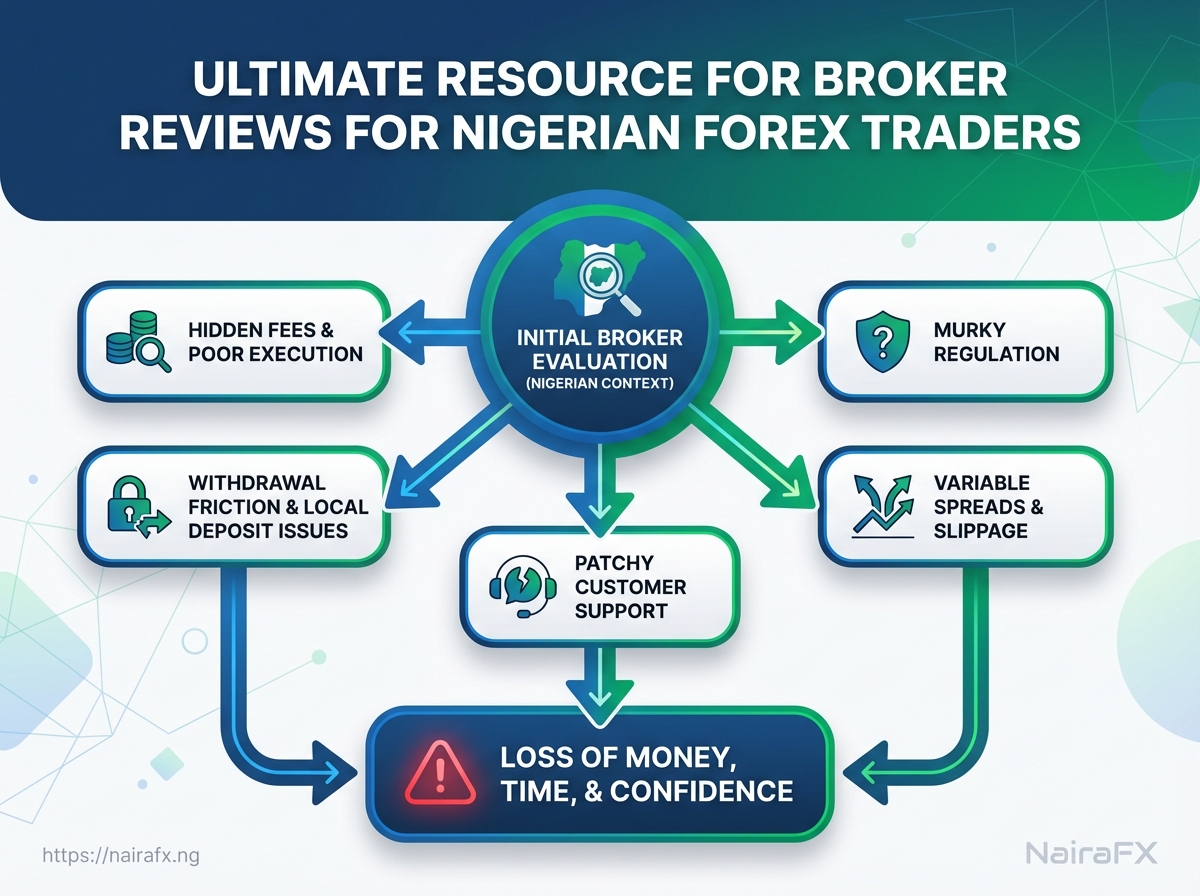

Most traders in Nigeria know the feeling: an account opens quickly, the dashboard looks slick, and only later do broker terms, hidden fees, or poor execution start eating profits. That delay between signup and real trouble is where many lose money, time, and confidence.

What confuses traders isn’t just price — it’s execution quality, withdrawal friction, local deposit routes, and the murky world of regulation that differs by jurisdiction. Add variable spreads, slippage, and patchy customer support, and comparing platforms becomes a guessing game rather than a practical decision.

Cutting through that noise requires simple, relevant checks that focus on how a platform behaves under real trading conditions, not marketing screenshots. The right comparisons protect trading capital and free up mental bandwidth for strategy, not platform firefighting.

How Forex Brokers Work and Why Choice Matters

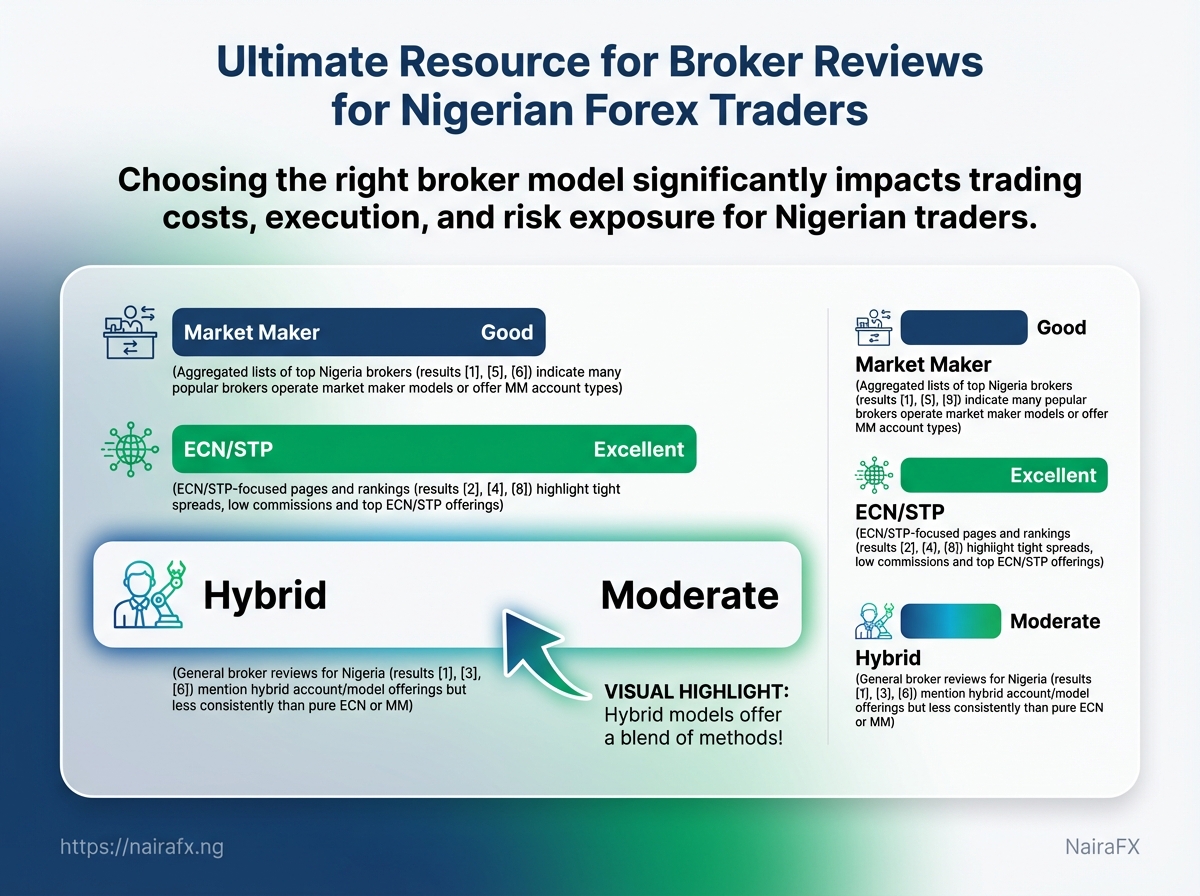

A broker is the plumbing between you and the market; the way that plumbing is built changes your costs, execution quality, and ultimately whether a strategy stays profitable under real conditions. Brokers either internalise order flow or pass it to interbank venues, and that design drives differences in price transparency, slippage, and conflicts of interest. Choosing poorly can turn a well-designed edge into a loser through hidden spreads, re-quotes, or slow fills — especially during Nigerian market hours when liquidity can thin.

Market Maker: A broker that often takes the opposite side of client trades and sets prices internally.

ECN/STP: Brokers that route orders to an Electronic Communication Network or Straight-Through Processing pools where prices come from multiple liquidity providers.

Hybrid: A broker that mixes internalisation with external routing depending on liquidity, size, or instrument.

Execution model affects price fairness and slippage in clear ways:

- Market makers can offer tighter advertised spreads but may widen them during volatility; slippage may be executed in-house.

ECN/STPmodels typically charge explicit commissions and show raw spreads from liquidity providers; slippage reflects true market movement.- Hybrids switch behavior dynamically, which can be good for retail clients but adds unpredictability for high-frequency strategies.

Typical cost components to model before risking capital:

- Spread: The difference between bid and ask; often wider at low liquidity or for exotic pairs.

- Commission: Per-lot charge common with

ECNmodels; sometimes bundled with spread. - Rollover (swap): Cost or credit for holding positions overnight; varies by pair and direction.

- Deposit/withdrawal fees: Banking and remittance charges can be material for traders in Nigeria.

How to test execution quickly: open a small live account, place market orders across different sessions, and compare fills to the raw interbank tick you capture via a data feed. Execution latency plus adverse slippage over many tiny trades compounds into measurable drag.

Side-by-side comparison of broker models and their pros/cons for Nigerian traders

| Feature | Market Maker | ECN/STP | Hybrid |

|---|---|---|---|

| Execution transparency | Low to medium — prices set internally | High — prices from multiple LPs | Medium — varies by instrument |

| Typical spread profile | Often tight on majors, widens in volatility | Raw spreads, often narrower pre-commission | Competitive but variable |

| Commission structure | Usually included in spread | Explicit per-lot commission | Mix of spread + occasional commission |

| Conflict of interest risk | Higher — broker may profit from client losses | Low — broker routes orders externally | Moderate — internalisation possible |

| Suitability for scalping/day trading | Mixed — some allow scalping, execution may be inconsistent | High — good fills, low latency | Depends on broker policy and routing |

Key insight: Market makers can be cost-effective for casual traders but demand careful due diligence on execution behaviour. ECN/STP suits active scalpers and strategy testing where reproducible fills matter; hybrids offer flexibility but require monitoring for when routing changes. Choose a broker whose execution profile matches the timeframes and instruments your strategy uses, and validate with real fills rather than relying on marketing spreads.

Picking the right broker isn’t academic — it changes realised returns. Test execution under live conditions and factor every fee into your model before scaling.

Regulation, Safety, and Risk Management for Nigerian Traders

Regulation isn’t optional—it’s the baseline that separates a gambling table from a professional market. Start by verifying a broker’s legal standing, insist on clear client-fund protections, and treat flashy marketing promises with deep skepticism. Proper checks reduce the chance of losing capital to fraud, bankruptcy, or opaque practices that quietly erode returns.

Where to verify a broker’s registration and license 1. Check the regulator’s public register for the broker name and licence number.

- Cross-check the broker’s registered business address against corporate registries in that jurisdiction.

- Confirm the licence type (retail dealer, investment firm, commodity broker) matches the services offered.

- Look for links to audited annual reports or third-party trust accounts confirming client fund segregation.

- Match the broker’s corporate registration (company number) to jurisdictional registries.

- Request a vendor bank statement or auditor confirmation showing

segregated client accounts. - If answers are evasive or documents are unverifiable, treat the broker as high-risk and avoid funding live accounts.

Regulatory checklist and red flags

License presence: Confirm a valid licence number on the regulator’s site.

Registered address: Verify a physical, verifiable corporate address—PO boxes alone are a red flag.

Segregated client accounts: Insist the broker keeps client funds separate from operating capital.

Audited financials: Presence of recent audit reports or proof of capital adequacy is a strong signal of transparency.

Compensation / investor protection scheme: Check whether the regulator offers deposit insurance or compensation for client losses if the firm fails.

Red flag — unrealistic promises: Guarantees of fixed high returns, “no-risk” claims, or pressure to deposit immediately.

Red flag — fake regulator references: References to non-existent rules, wrong licence types, or logos that don’t match official regulator branding.

Practical verification steps 1. Search the regulator directory for the exact legal entity name and licence number.

Regulatory features (license, client fund segregation, compensation scheme) across regulator types

| Regulatory Feature | Tier-1 Regulators | Tier-2 Regulators | Unregulated/High-risk |

|---|---|---|---|

| License verification ease | High — public searchable registers (FCA, ASIC, FINMA) | Moderate — public registers but varying detail (CySEC, FSCA) | Low — no authoritative register |

| Client fund protection | Strong — segregation rules, frequent audits | Variable — segregation often required, enforcement varies | None — client funds at operator risk |

| Capital requirements | High — substantial minimum capital levels | Moderate — lower minimums than Tier-1 | None |

| Investor compensation scheme | Yes — formal schemes exist in many Tier-1 jurisdictions | Limited/Optional — smaller compensation limits | No |

| Enforcement track record | Robust — regular sanctions and published enforcement actions | Mixed — enforcement slower, resources smaller | Absent |

Key insight: Tier-1 regulators provide the clearest public protections and enforcement history, Tier-2 regulators offer reasonable protections but with variability, and unregulated operators present material counterparty risk.

Choosing brokers this way reduces exposure to fraud and operational failure, and it makes risk management predictable rather than hopeful. Take the few extra minutes to verify licences and segregation—those checks protect both capital and mental bandwidth when markets get noisy.

Practical Evaluation Criteria: Fees, Execution, and Platforms

Start by scoring brokers against the few things that actually move profits: fees, execution quality, and how easy it is to move Naira in and out. A simple weighted scorecard lets those tradeoffs become objective instead of emotional—weight criteria to match your trading style and test execution with small live runs before committing capital.

Scoring framework (example weights)

Style weightings: Scalper/EA: Speed 35% | Spread/Commission 30% | Platform features 20% | Local deposits 15% Swing trader: Spread/Commission 30% | Platform features 30% | Speed 20% | Local deposits 20% Position trader: Platform features 35% | Spread/Commission 25% | Local deposits 25% | Speed 15%

How to measure execution (practical steps)

1. Backtest latency-adjusted: Run historical fills with slippage parameters that reflect published average execution times.

2. Micro live test: Deposit a small funded amount and run 50–200 round-trip trades during typical market hours.

3. Measure and log: Track average fill price vs. quoted price, order rejections, and round-trip time in ms.

4. Aggregate: Calculate execution score from fill slippage (points for <0.2 pips slippage), rejection rate, and consistency.

Important local-deposit considerations

Local bank transfer: Fast, low cost, preferred for Naira liquidity. Payment processors (Skrill, Neteller): Quicker than some banks but may add conversion fees. Crypto rails: Useful when banking lanes are unstable; watch volatility and on/off ramp fees.

Sample broker scorecard comparing key metrics and final score

| Metric | Broker A (sample) | Broker B (sample) | |

|---|---|---|---|

| Spread (pips) | Typical EUR/USD spread during London session | 0.8 | 1.4 |

| Commission (per lot) | Round-turn commission on major FX lot | $3.5 | $0 |

| Avg. execution speed (ms) | Measured average order-to-fill time from micro-tests | 45 ms | 220 ms |

| Platform uptime (%) | 30-day reported uptime during trading hours | 99.98% | 99.70% |

| Local deposit options | Naira bank transfer / Skrill / Crypto support | Naira bank transfer ✓ / Skrill ✓ / Crypto ✓ | Naira bank transfer ✗ / Skrill ✓ / Crypto ✓ |

Key insight: Broker A suits scalpers and EAs because of low spreads, low commission, and fast execution; Broker B may be cheaper for commission-free traders but has slower fills and lacks direct Naira bank transfer, which adds friction for Nigerian traders.

Choose weights that mirror how often you trade and how sensitive your strategy is to tiny slippage. Run the micro live tests described above, plug results into the scorecard, and the trade-offs will usually be obvious.

📝 Test Your Knowledge

Take this quick quiz to reinforce what you’ve learned.

Deposit, Withdrawal, and Currency Considerations for Nigerian Traders

Nigerian traders need to plan deposits and withdrawals with the same care given to entry and exit rules. Payment rails, conversion costs, and documentation timelines directly affect how much capital actually reaches a broker, how fast trades can be funded, and how quickly profits return to your wallet. Below are practical mechanics, examples of common friction points, and concrete steps to speed approvals and reduce currency drag.

Local payment rails and how they bite into capital Local bank transfers (Naira): Cheap or free within Nigeria, but many international brokers require conversion to USD/EUR on deposit or their local Naira bridge — expect spread-based conversion rather than transparent FX rates. SWIFT (USD/EUR): Reliable for sending hard currency but attracts sending bank fees (often $20–$40), intermediary bank fees, and receiving bank charges — total cost can be 0.5–2% of the transfer plus fixed fees. Payment processors (Skrill, Neteller): Fast and often lower transfer fees for inbound deposits; however, withdrawal options and payout currencies vary per broker and processor. Crypto (USDT, BTC): Very fast and typically lower fees when using USDT on TRC20; price volatility and exchange on/off ramps to Naira are the main risks. * Card payments (Visa/Mastercard): Instant funding but card networks or banks may block FX transactions, and brokers often add a 1–3% fee.

How currency conversion affects trading capital Conversion spreads and double-conversion fees can silently erode position size. If a Naira deposit is converted to USD at an unfavorable rate, the effective buying power drops before a single trade is placed. Hedging via stablecoin deposits or using brokers that accept Naira accounts can preserve capital if the broker’s FX markup is lower than local bank spreads.

Documentation and speeding withdrawals 1. Upload all KYC documents (valid ID, proof of address, and a bank statement) before funding to avoid hold-ups. 2. Provide transaction proof (bank transfer screenshot or payment processor invoice) immediately after deposit to link funds to your account. 3. When withdrawing, confirm the exact beneficiary details and any intermediary bank instructions to avoid return delays.

Deposit/withdrawal methods by cost, speed, and typical availability for Nigerian traders

| Method | Typical Fees | Typical Speed | Availability (Nigeria) |

|---|---|---|---|

| Local bank transfer (Naira) | Low to none on domestic side; broker FX spread 0.5–3% | 1–3 business days | Widely available |

| SWIFT (USD/EUR) | $20–$40 send + intermediary fees; broker receiving fees possible | 2–5 business days | Available via major banks |

| Payment processors (Skrill, Neteller) | 0.5–2% common; instant internal transfers | Instant to 24 hours | Popular but not universal |

| Crypto (USDT, BTC) | Network fees: <$1 (TRC20 USDT) to several dollars; exchange conversion fees apply | Minutes to hours | Growing availability; needs local on/off ramps |

| Card payments (Visa/Mastercard) | 1–3% + possible bank FX markup | Instant | Widely available but sometimes blocked for FX purchases |

Key insight: Brokers and payment rails differ widely — using stablecoins or payment processors often reduces FX drag and speeds funding, while SWIFT offers broad acceptance at higher predictable cost.

Practical habits that matter: check your broker’s cashier page for accepted Naira options, compare their displayed FX rate against market mid-rates, and pre-verify accounts before large transfers. Getting these operational bits right keeps more capital in play and avoids frustrating withdrawal delays.

Types of Brokers and Best Fits for Nigerian Trader Personas

Matching a trader to the right broker comes down to aligning trading style with execution, costs, and reliability. Scalpers need ultra-low latency and tight spreads; position traders want deep liquidity and robust research; algorithmic traders require stable APIs and VPS support. Below is a practical guide that maps common Nigerian trader personas to the broker features that matter most, plus what to watch out for when negotiating terms or verifying claims.

Map trader personas to priority broker features

| Persona | Top 1-2 Broker Priorities | Secondary Priorities | Red flags for this persona |

|---|---|---|---|

| Scalper | Low spreads & fast execution | Commission transparency, micro-lot support | Re-quotes, slowed execution during news |

| Swing trader | Reasonable spreads & reliable order fills | Charting tools, margin flexibility | High overnight swap costs, thin liquidity on majors |

| Position trader/Investor | Regulatory safeguards & deep liquidity | Research access, dividend handling | Unclear custody, no segregated client accounts |

| Algorithmic/EA trader | Stable API / MT5/MT4 bridge | VPS access, backtest data | Frequent server downtime, limited API rate limits |

| Beginner | Simple onboarding & educational support | Demo accounts, low minimum deposit | Overly aggressive marketing, complex fee waterfalls |

Industry analysis shows these matchups repeat across forums and broker docs: latency and spreads dominate for scalpers; regulation and custody matter for long-term investors; uptime and API access make or break automated strategies. When evaluating brokers:

- Verify execution claims: Ask for real-time demo with your routine (open/close during news).

- Check withdrawals: Perform a small live deposit and withdrawal to test KYC and payout speed.

- Prioritise tradeoffs: If tight cost is critical, expect fewer client protections; if safety is priority, budget for slightly higher spreads.

Practical negotiation tip: request a written SLA for execution speed or a demo account tied to the live environment; brokers often accommodate serious, funded accounts.

Choosing the right broker reduces friction and preserves edge. Pick the features that matter most to your style, confirm them with live tests, and treat regulatory safeguards as non-negotiable for longer-term capital protection.

How to Run Your Own Broker Review and Stay Updated

Start by treating broker reviews as living documents that you update on a schedule. A short, repeatable process prevents surprises: run quick functional checks each month, deeper compliance and financial checks quarterly, and keep automated monitors running continuously. That way trading quality and counterparty risk stay visible without eating all your time.

Monthly maintenance checklist

- Execute a small live trade batch (paper or micro) and inspect fills.

- Verify withdrawal path by making a withdrawal of a small amount.

- Test support response time and ticket quality.

- Run a latency test during peak hours and off-peak hours.

- Reconcile

trade logswith your broker’s execution reports.

- Execution test: Place

5-10small trades across different instruments to check slippage and fills. - Withdrawal test: Use the same method your traders use and confirm funds arrive within declared times.

- Support check: Open a ticket, ask a technical question, note time-to-first-response and resolution quality.

Quarterly checks and deeper monitoring

- Terms and policy review: Compare current T&Cs to previous versions for changes to fees, margin, or order handling.

- Regulatory watch: Scan regulator announcements for enforcement actions or license changes.

- Financial review: Read available financial statements or parent-company reports for solvency signals.

- Market-quality comparison: Run a price-feed comparison against at least two other brokers or an exchange.

Tools for ongoing monitoring

- Trade logs: Export and store raw execution data daily for reconciliation and pattern analysis.

- Latency tester: Use simple TCP/ICMP tools or dedicated market latency services; flag deviations >

100ms. - Price comparison feed: Pull quotes from your broker and independent sources to detect stale or lagged pricing.

- Automated alerting: Configure alerts for spikes in slippage, rejection rates, or support response lapses.

- Analytics sandbox: Use Monte Carlo or scenario testing to see how changes in fills/slippage affect your strategy returns.

Follow this step-by-step process each cycle:

- Run the monthly checklist and log results.

- Trigger automated monitors and review alerts.

- Perform quarterly deep checks and update your review document.

- If any test fails, escalate to the broker with evidence and repeat tests after resolution.

Keeping a disciplined schedule and simple automated tooling lets you spot degradation before it harms P&L. Regular, lightweight checks are far more effective than infrequent, exhaustive audits — and they save time while keeping trading risks visible.

📥 Download: Forex Broker Evaluation Checklist for Nigerian Traders (PDF)

Case Studies and Sample Broker Reviews

Three short, concrete case studies show how a scoring framework turns raw experience into actionable guidance for Nigerian traders. Each review below uses a consistent rubric—liquidity/execution, regulatory footprint, deposit/withdrawal reliability, and customer support—scored out of 100. The examples explain what to watch for, how scores map to decisions, and when to escalate problems to regulators or dispute resolution.

Common signals to watch while following a recommendation: Execution lag: Noticeable slippage or order re-quotes during news—document timestamps and ticket IDs. Withdrawal friction: Repeated delays, extra KYC requests, or unexpected fees after withdrawal requests. * Regulatory mismatch: Claimed licences that don’t match the regulator register or using offshore entities without clear consumer protections.

Side-by-side summary of the three sample broker reviews with scores and recommendation

| Aspect | Broker (Recommended) | Broker (Conditional) | Broker (Avoid) |

|---|---|---|---|

| Overall score | 88/100 | 68/100 | 34/100 |

| Regulatory status | Licensed by FCA-equivalent regulator; clear legal entity | Offshore licence with limited consumer protection | No verifiable licence; anonymous corporate structure |

| Withdrawal experience | Fast (24–72 hrs), clear fees | Usually processed; occasional 5–7 day delays | Withdrawals often stalled >14 days; repeated rejection |

| Execution/spread experience | Tight spreads, low slippage; ECN options | Variable spreads during news; some slippage | Wide spreads, frequent requotes and requotes |

| Final recommendation | Recommended for live accounts; good for position and intraday traders | Use with small live size; monitor withdrawals closely | Avoid — escalate if funds blocked; only paper trade if at all |

How the scoring framework produces actionable guidance: Score bands: 80–100 = recommended; 60–79 = conditional; <60 = avoid. Concrete watchpoints: Save screenshots for execution problems; keep withdrawal emails in a single folder; note the account manager name and timestamps. * Escalation triggers: Funds not released in 14 days, contradictory licence claims, or evidence of client fund commingling.

When to escalate 1. Document everything: screenshots, timestamps, transaction IDs. 2. Contact broker support and request a written timeline. 3. If unresolved after 7–14 days, file a complaint with the broker’s regulator and open a dispute via payment provider.

These examples show how a repeatable score and simple documentation habits turn anecdote into evidence — making disputes more effective and day-to-day broker choices clearer for Nigerian traders.

Conclusion

Most Nigerian traders start with a shiny dashboard and only later notice spreads, execution gaps, or withdrawal hold-ups eating their edge. Recall the case where a scalper switched to a low-latency ECN account and halved slippage, or the review that exposed recurring withdrawal fees that turned profits into losses—those are the sorts of practical differences that matter every trade. Prioritise regulated brokers, test execution with a live micro account, and track real deposit/withdrawal timelines before committing capital. If you’re unsure how a broker stacks up on those fronts, the NairaFX broker comparison guide lays out side-by-side checks and recent review notes to speed that decision.

Next steps: open a small live account to verify execution and withdrawals, keep a running log of fills and charges for 30 trades, and revisit regulation status every quarter. Common questions — like “can I use naira deposits?” or “how do I verify an FCA/ASIC licence?” — are answered in the platform’s FAQ and the linked guides, but the practical test above settles most doubts faster than promises on a landing page. Act deliberately: test with real money, document outcomes, then scale. That discipline separates stories of frustration from consistent trading results.