Most Nigerian traders open accounts with shiny websites and flashy spreads, then discover withdrawals stall, slippage eats profits, or customer support goes quiet when markets move. Choosing a reliable forex broker is less about the lowest spread and more about how they handle volatility, regulatory pressure, and payout friction during real trades.

Spotting those warning signs before funding an account is a skill that saves money and sleepless nights. Practical checks — from document transparency to order execution evidence and funding routes — separate brokers that behave predictably from those that don’t.

Executive Summary

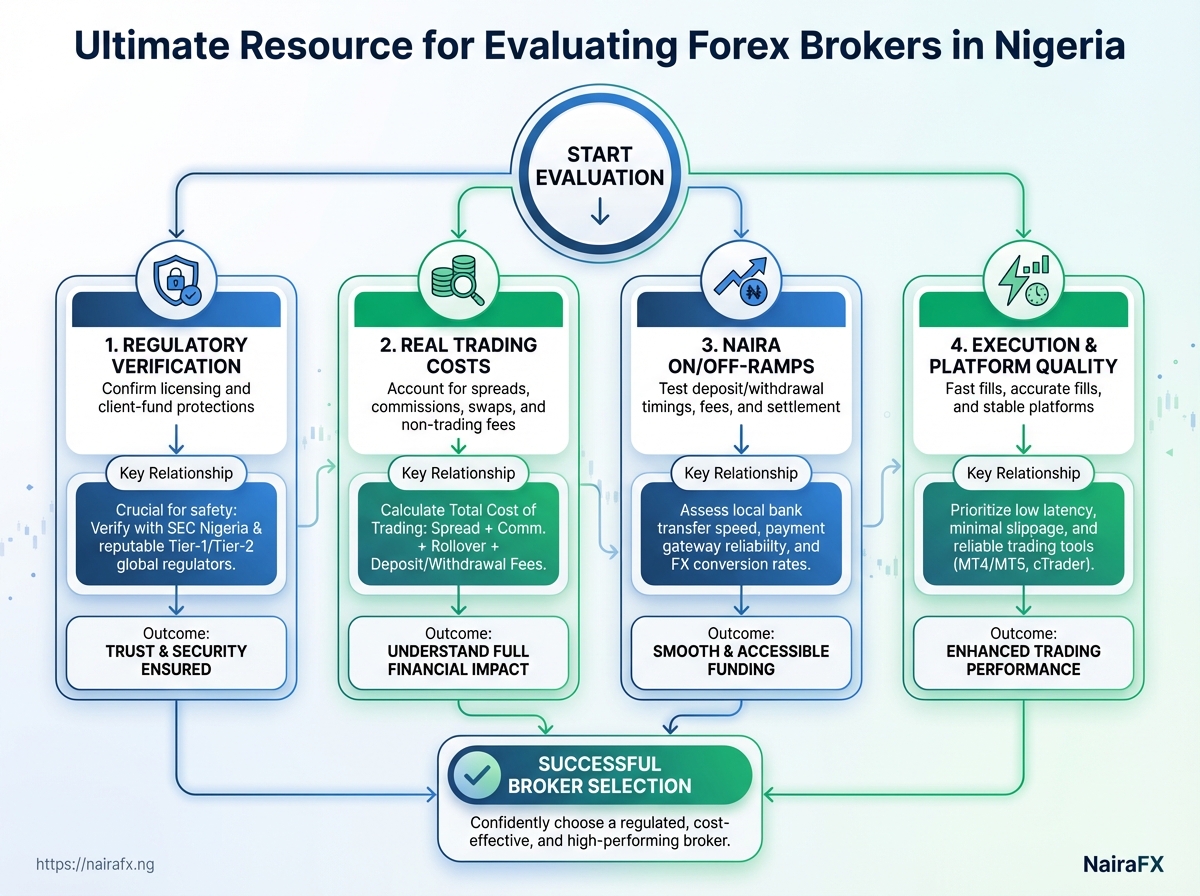

For Nigerian traders navigating volatile FX and equities markets, the practical priorities are simple and immediately actionable: confirm a broker’s regulatory standing, know the full cost of trading, verify on- and off-ramp performance in naira, and choose execution-focused platforms. These four moves cut the most common sources of loss — not market noise, but avoidable friction and counterparty risk.

Start by treating regulatory checks as non-negotiable. Many reputable firms list their license, complaints process and local payment partners; verify those before funding an account.

Regulatory verification: Confirm licensing, complaints procedures, and the broker’s client-fund protections before any deposit.

Understand that headline spreads are only part of the cost story. Real cost includes spread, commissions, swap (overnight financing) and non-trading fees such as withdrawal charges, currency conversion margins and inactivity fees. Run a simple break-even calculation on a trade horizon to see how those costs erode returns.

Real cost: Spread + commissions + swaps + non-trading fees — price them per-trade and as a percentage of typical position size.

Test deposits and withdrawals in naira as a practical litmus test. A broker that shows fast, predictable on/off ramps with low conversion slippage will preserve capital and reduce operational stress when repatriating profits.

Test deposits/withdrawals: Use a small live deposit and withdrawal in naira to verify timings, fees, and settlement issues before scaling up.

Prioritize brokers offering low-latency execution, transparent price feeds and robust platforms — not flashy bonus offers. Execution quality beats exotic features when markets move fast; insist on measurable order-fill stats or demo-to-live slippage comparisons.

Execution & platform: Fast fills, accurate fills, and stable platforms reduce slippage and emotional errors in volatile markets.

Practical next steps

- Check regulatory details and complaint records, then document them.

- Price a representative trade including

spread, commission, swap, and withdrawal costs. - Make a small naira deposit and withdrawal; record timings and fees.

- Compare execution by placing mirror demo and small live trades, tracking slippage.

For systematic traders, running a Monte Carlo simulation on your equity curve and transaction costs exposes tail risks and position-sizing flaws early; services that model execution and swaps are especially helpful. Try these checks before increasing exposure — they save both capital and time when markets get choppy.

How to Verify Broker Regulation and Safety

Start by treating a broker’s claim of regulation as a starting point, not proof. Regulators vary widely in oversight intensity and protections. Confirm the regulator, check the licence number on the regulator’s public register, and ask the broker for verifiable corporate documents. Do this before funding an account — it’s the difference between recoverable losses and losses that vanish into thin air.

What regulators matter and why

Tier-1 regulators: Strong supervision, strict capital requirements, regular audits, and enforceable client protections. Tier-2 regulators: Moderate oversight, useful for some businesses but lower consumer protection. Unregulated / Offshore labels: Frequently used to evade rules; treat them with high suspicion.

Step-by-step: How to verify a broker’s licence

- Visit the regulator’s official public register.

- Enter the broker’s legal company name or the provided licence number (for example,

LIC-123456). - Confirm registered address, licence status (active/suspended), and scope (e.g., derivatives, forex).

- Cross-check company registration information with national corporate registries.

- If anything is missing or the register shows a different legal name, do not proceed with deposits.

Documents to request from the broker

Corporate registration: Certified extract showing legal entity name and registration number.

Regulatory licence certificate: Scanned copy showing licence number and scope of permission.

AML/KYC policy: Clear description of client verification, transaction monitoring, and suspicious-activity processes.

Proof of segregated accounts: Bank statements or bank letter confirming client funds are held separately from the broker’s operating accounts.

Complaints and compensation procedures: Document describing how client complaints are handled and whether a compensation scheme covers clients.

Practical checks and red flags

- Confirm domain ownership: The broker’s domain WHOIS should match the corporate details where possible.

- Ask for regulator contact: Call or email the regulator’s published contact to confirm the licence — regulators can and do confirm legitimacy.

- Watch for generic documents: Photocopied licences, screenshots, or documents without verifiable reference numbers are suspicious.

Side-by-side comparison of major global regulators and what protections they provide to retail traders

| Regulator | Jurisdiction | Typical Protections (segregation, compensation schemes) | Suitability for Nigerian traders |

|---|---|---|---|

| FCA | United Kingdom | Segregated client accounts, Financial Services Compensation Scheme (FSCS) up to £85,000 in certain cases, strict AML and reporting | High — strong investor protections; widely trusted |

| CySEC | Cyprus / EU | Client fund segregation, Investor Compensation Fund (limited), EU passporting rules | Moderate — common for EU access; protections present but smaller compensation caps |

| ASIC | Australia | Client money rules, limited compensation, strict licensing and enforcement | High — robust oversight, good for institutional-style protections |

| NFA | United States | Segregation via FCM rules, strict reporting, CFTC oversight (no direct retail OTC forex for some entities) | Moderate — strong enforcement but complex for retail forex access |

| CBN (local oversight — payments only) | Nigeria | Oversight of payment systems and local fx settlements, not a full forex broker licensing regime | Limited — useful for payments/collections but not sufficient as sole proof of broker safety |

Key insight: Stronger regulators (FCA, ASIC) offer more enforceable protections; CySEC and NFA have meaningful rules but different scopes; CBN mainly governs payment rails, not full broker licensing.

Trust but verify — a verified licence on a regulator’s public register, plus corporate registration and segregated-account proof, should be the minimum before transferring funds.

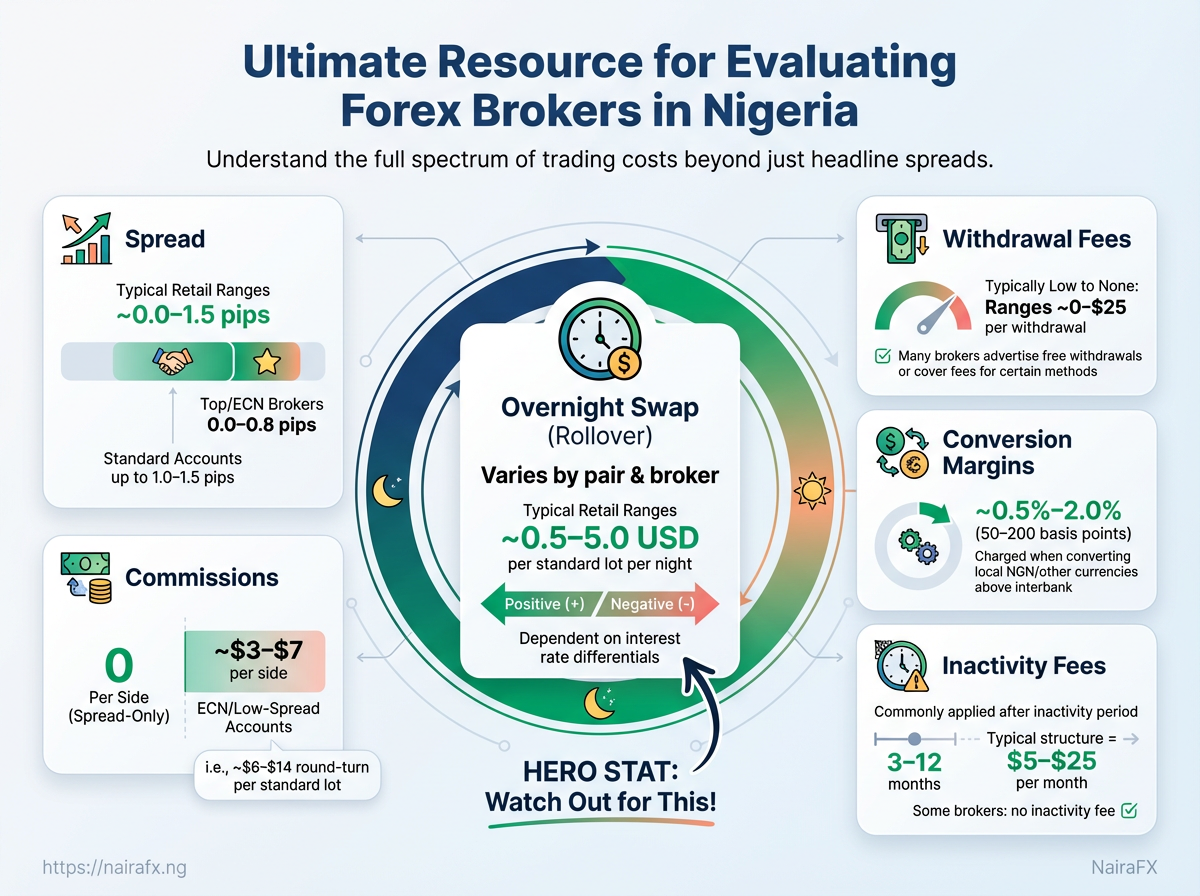

Trading Costs: Spreads, Commissions, Swaps and Hidden Fees

Think of trading costs as the invisible drag on returns — small each trade, large over time. True cost combines several moving parts: what the market charges via the spread, explicit commissions, overnight swap interest adjustments, and non-trading fees (deposits, withdrawals, inactivity). For a Nigerian trader converting Naira to USD or using naira-denominated accounts, currency conversion and local bank charges can turn a cheap-looking broker into an expensive one.

Spread: The difference between bid and ask; paid every trade as pips × pip value. Commission: Fixed or per-lot fee charged by some account types; often shown per side. Swap: Interest earned or paid for holding positions overnight; can be positive or negative. Non-trading fee: Deposit/withdrawal charges, conversion costs, inactivity and data fees.

How to calculate an all-in cost for a single round-trip 1 standard lot = 100,000 units trade: Start with spread cost: spread (pips) × $10 for most major pairs per lot. Add explicit commissions: include both entry and exit if charged per side. Include swap: estimate per-night swap and multiply by nights held. Add non-trading fees: bank charges and conversion fees when depositing Naira to USD.

Illustrate a worked example comparing total cost breakdowns for two account models (spread-only vs commission) for a 1 standard lot round-trip trade

| Cost Component | Spread-based account (USD) | Commission-based account (USD) | Notes |

|---|---|---|---|

| Spread cost | $12.00 | $2.00 | Assumes 1.2 pips vs 0.2 pips; $10 per pip per lot |

| Broker commission | $0.00 | $14.00 | Commission $7 per side on commission model |

| Swap (overnight) for 1 night | $5.00 | $5.00 | Example negative swap charged ≈ $5 for 1 night |

| Deposit/withdrawal fee | $25.00 | $25.00 | Bank conversion and remittance fees (Naira→USD) |

| Total round-trip cost | $42.00 | $46.00 | All components combined for 1-night hold |

Key insight: The cheaper spread isn’t always cheaper after commissions and bank fees; swaps add material cost for carry trades and multi-night holds.

Practical note: for scalping, a low-spread account often wins. For multi-day position trading, compare swaps and local conversion fees — a seemingly higher-commission account can be cheaper overall. Keep a simple spreadsheet to calculate all-in cost before committing significant position size.

Execution Quality, Slippage and Order Types

Execution quality matters more than strategy if orders don’t fill where expected. Start by testing live fills against quoted prices and capturing time-to-fill, fill rate, and the size of price movement between order submission and execution. Doing this repeatedly during different market conditions reveals whether a broker’s execution is reliable or quietly costly.

What to test and how Measure quoted vs executed price: Place market and limit orders and record the price quoted at submission and the price executed. Capture timestamp and trade size. Track fill rate: Count the number of orders fully filled vs partially filled or rejected over 100+ trades. Time-to-fill: Measure latency from order submission to execution in milliseconds for smaller traders; note execution times in seconds during news. Requote frequency: Record how often the broker refuses a price and offers a new one. * Order-type behaviour: Test market, limit, stop, stop-limit, and trailing orders to confirm they behave as documented.

Step-by-step live test

- Fund a demo or micro-account with realistic size.

- Place 100 balanced orders across quiet hours, volatile sessions, and news spikes.

- Log: submission price, executed price, timestamp, size, and whether partial fill/requote occurred.

- Calculate average slippage, fill rate, and latency.

Acceptable slippage thresholds for retail traders 0–0.5 pip on major FX pairs during normal market conditions is typical for competitive ECN/STP execution. 0.5–1.5 pips may be reasonable for less-liquid pairs or during moderate volatility. * >2 pips regularly on majors signals an execution problem or hidden mark-up.

Common manipulative behaviours and warning signs Frequent requotes during normal volatility — can indicate internalized order flow or latency arbitrage against you. Consistent one-sided slippage (always worse than quoted) — suggests movement by the broker rather than market spread widening. * Hidden order rejections on large sizes but fills on smaller ones — points to size-based withholding or bucket shops.

Checklist matrix for execution-related features and metrics to compare across brokers

| Metric/Feature | How to measure | Good benchmark | Why it matters |

|---|---|---|---|

| Average slippage | Mean difference between quoted and executed price across 100 trades | ≤0.5 pip (majors, calm) | Direct transaction cost; erodes edge |

| Fill rate | % of orders filled fully out of total orders | ≥99% | Partial fills cause execution uncertainty |

| Requote frequency | % of orders requoted before fill | <0.1% | High requotes indicate poor liquidity handling |

| Order types supported | Test all documented order types for expected behaviour | Full support for market/limit/stop/stop-limit/trailing | Strategy flexibility depends on true order behaviour |

| Execution model (STP/ECN/MM) | Review policy + empirical tests for slippage/quotes | ECN/STP with DMA preferred | Model affects conflict of interest and execution path |

Key insight: Testing execution under live conditions exposes lightweight costs—slippage, latency, and fills—that backtests ignore. Run small, repeatable experiments and compare brokers with the checklist above to ensure execution doesn’t quietly eat strategy returns.

Good execution habits pay off: a consistent, repeatable testing discipline turns invisible costs into controllable variables.

Trading Platforms, Tools and Technology

Choose a trading platform the way you’d choose a toolbox: reliability first, features that match your workflow second. For active traders in Nigeria, a platform that delivers clean historical tick data, stable execution, and a usable API/VPS combo makes the difference between a strategy that scales and one that collapses under latency and data gaps. Mobile apps should feel like the desktop, not an afterthought — parity matters when markets move while you’re away from your desk.

What to prioritize when evaluating platforms

- Reliability and uptime: Look for platforms with proven low-latency routing and redundant servers.

- Historical tick data access: High-resolution tick data enables realistic backtests and accurate slippage modeling.

- API support and protocols:

RESTandWebSocketaccess plus good SDKs reduce engineering overhead. - VPS integration or colocated hosting options: Keeps automated strategies running during local connectivity issues.

- Order types and execution controls: Good platforms offer advanced order types, partial-fills control, and pre-trade risk limits.

- Mobile/Desktop feature parity: The trading experience must be consistent across devices to avoid decision gaps.

- Reporting and exportability: Easy exports of fills, market data, and trade logs for reconciliation and performance analysis.

s

API: Programmatic interface for sending orders, streaming data, and fetching account state.

VPS: Virtual private server used to host bots close to exchange endpoints to reduce latency.

Historical tick data: Millisecond-level recorded trades and quotes used for precise backtesting.

How to evaluate a platform — quick checklist

- Confirm historical tick data availability and sample a dataset for your instruments.

- Test the public API: fetch real-time quotes, place/cancel simulated orders, and measure response times.

- Run a short automated strategy on a VPS for 24–72 hours to observe stability under live conditions.

- Compare mobile and desktop flows by performing identical tasks on both and noting missing controls.

Practical example: run a Monte Carlo stress test on locally captured tick data before going live to see how tail events affect drawdowns; this integrates directly with risk evaluation workflows used in position-sizing services.

Choosing the right stack pays for itself: fewer execution surprises, cleaner analytics, and a smoother transition from backtest to live trading. Keep the focus on data fidelity, automation robustness, and consistent UX across devices — those three will save more time and capital than chasing bells and whistles.

📝 Test Your Knowledge

Take this quick quiz to reinforce what you’ve learned.

Account Types, Funding, Withdrawals and Local Considerations

Most brokers offer similar retail account types—standard, mini/micro, and professional—but the practical constraints for Nigerian traders often come down to how you fund and withdraw. Confirm whether a broker accepts NGN directly or only converts through a partner; that single detail changes costs, speed and compliance requirements. Start small when testing a new broker: one tiny deposit and one small withdrawal proves the rails before you scale capital.

Practical funding and withdrawal guidance for Nigeria

Account setup: Complete KYC early; brokers will ask for a valid ID, recent utility bill and sometimes a proof-of-funds document for larger deposits. Test transactions: Make a small NGN deposit, then withdraw the same amount to verify limits, fees and processing times. Conversion awareness: If a broker doesn’t support NGN, expect their partner or your bank to convert — and to apply FX spreads and fees. Recordkeeping: Keep screenshots of deposit forms, SWIFT receipts and payment processor confirmations for disputes or proof-of-funds requests.

Funding methods and practical tips for Nigeria

Funding and withdrawal methods available to Nigerian traders across key attributes (speed, typical fee, FX risk, convenience)

| Method | Typical Processing Time | Typical Fees | FX Exposure | Notes for Nigeria |

|---|---|---|---|---|

| Local bank transfer (Naira) | 1–3 business days | Low to moderate (₦100–₦2,000 local fees) | Low if broker accepts NGN; otherwise medium-high |

Best when broker supports NGN; avoids SWIFT fees and reduces FX spread |

| Payment processors (Paystack/Flutterwave equivalents) | Minutes to 1 business day | Moderate (1%–3% + fixed fee) | Medium (often converted by processor) | Convenient and fast; check processor limits and chargebacks policy |

| SWIFT international bank transfer | 3–7 business days | High (bank fees ₦2,000–₦10,000 + correspondent fees) | High (conversion by receiving bank) | Reliable for large transfers but costly; keep SWIFT copy for withdrawals |

| Credit/debit card | Instant to 1 business day | Moderate (1.5%–4% + possible cash advance fees) | Medium (card issuer converts) | Fast and convenient; some brokers charge extra for card withdrawals |

| E-wallets (Skrill/Neteller) | Instant to 1 business day | Moderate (deposit often free; withdrawal fees apply) | Medium (wallet conversion) | Good for speed and privacy; set up and verify accounts before funding |

Key insight: Local bank transfers and Nigerian payment processors offer the best balance of cost and convenience when brokers support NGN. SWIFT is a fallback for large sums but carries notable fees and FX risk.

Follow-up actions that save time: confirm NGN support before account opening, test small deposits and withdrawals, and document every transaction. These small steps prevent costly surprises and keep your trading capital accessible when markets move.

Comparison Framework and Sample Broker Matrix

A simple, repeatable scoring model removes emotion from broker selection and makes tradeoffs explicit. Use four core categories, assign default weights based on Nigerian traders’ priorities, then score each broker on a 0–10 scale. The result is a ranked matrix you can tweak for different strategies (scalping, swing, position trading).

Scoring categories and default weights

Regulation & Safety: 30% Total Cost: 25% Execution Quality: 25% Local Funding/Support: 20%

How overall scores are calculated

- Score each category 0–10 for a broker.

- Multiply each score by its weight (weight expressed as decimal).

- Sum the weighted values to get the overall score (max 10).

Example: If a broker scores 8 in Regulation, 7 in Cost, 9 in Execution, 6 in Local Support: 1. (8 0.30) = 2.4 2. (7 0.25) = 1.75 3. (9 0.25) = 2.25 4. (6 0.20) = 1.2 Total = 7.6 /10

Sample broker scoring matrix to rank brokers across critical evaluation categories

| Broker (archetype) | Regulation & Safety (score) | Total Cost (score) | Execution Quality (score) | Local Funding/Support (score) | Overall score |

|---|---|---|---|---|---|

| Broker A – Low-cost ECN | 7 | 9 | 8 | 5 | 7.7 |

| Broker B – Market maker with NG support | 6 | 7 | 7 | 9 | 7.1 |

| Broker C – Tier-1 global | 9 | 5 | 9 | 6 | 7.6 |

| Broker D – Crypto-friendly broker | 5 | 8 | 6 | 4 | 6.1 |

| Broker E – Emerging offshore | 4 | 6 | 5 | 3 | 4.7 |

Interpretation notes: higher overall score favors safer, well-executed trading conditions; Broker A ranks top for cost-sensitive traders, Broker C is strongest on safety and execution, Broker B wins when local support matters.

Adjust weights for different strategies

- Scalpers: Increase Execution Quality to 40%, reduce Regulation to 20%, keep Total Cost at 30%, Local Support 10%.

- Swing traders: Raise Regulation & Safety to 35%, Local Funding/Support to 25%, lower Execution to 20%, Total Cost 20%.

- Position traders: Emphasize Regulation & Safety 40%, Local Support 25%, Total Cost 20%, Execution 15%.

Practical next steps: run the matrix with live quotes and deposit options before committing funds, then re-score every 6–12 months as fees, regulations and local banking options change. This method keeps broker selection measurable and aligned with how you actually trade.

Risk Management, Leverage and Account Protection

Leverage amplifies both profits and losses, so treating it like a dangerous tool rather than free money is essential. Use leverage to fine-tune position size, never to chase returns; the simplest rule: if you’d lose sleep at a 5% drawdown, your leverage is probably too high.

Putting the math in plain terms helps. If account equity is ₦500,000 and a broker offers 100:1 leverage, ₦500,000 controls ₦50,000,000 notional. A 1% move on that notional equals ₦500,000 — a full loss of equity. Contrast that with 10:1 leverage: ₦500,000 controls ₦5,000,000; a 1% move is ₦50,000 — a manageable hit within risk limits.

Practical leverage examples: High leverage (100:1): One adverse 1% swing wipes ~100% of equity. Moderate leverage (20:1): One adverse 5% swing hits ~100% of equity. * Low leverage (5:1): Allows bigger market swings before capital exhaustion.

Protective policies every trader should check before funding an account: Negative balance protection: Ensures the trader cannot lose more than deposited.

Margin call level: The equity percentage where the broker starts restricting new trades.

Stop-out level: The equity percentage where the broker begins closing positions automatically.

Guaranteed stop-loss availability: Confirms stops execute at the requested price, often for an extra fee.

Execution model (ECN vs Market Maker): Affects slippage and conflict-of-interest risk.

Recommended leverage caps for retail Nigerian traders: Beginners: cap at 5:1 to 10:1 — focus on trade selection and consistency. Intermediate traders with solid risk controls: 10:1 to 20:1. * Experienced, well-diversified traders: up to 30:1 only with strict position-sizing rules.

Position-sizing rule to use immediately: risk no more than 1–2% of account equity per trade. For a ₦500,000 account and 1% risk, maximum loss per trade is ₦5,000 — size the position so a stop-loss equals that amount.

Risk tools and audits to adopt: regular equity-curve reviews and drawdown tracking, Monte Carlo simulation to stress-test strategy robustness (useful for longer-term traders), * an emergency kill-switch: a manual stop to close all positions if automated rules fail.

Treat leverage as a scaling knob, not a performance hack, and verify account protections before you trade. The right caps and protections keep trading a sustainable business rather than a series of avoidable crises.

Quick Reference Cheat Sheet

Start by checking the essentials that reveal whether a broker will behave predictably under stress. Use this sheet as a one-page printout during account setup and the first two weeks of live interaction — it separates immediate red flags from features you can test over time.

Printable checklist — immediate verification (must-check)

- Regulation & license: Confirm regulatory body, license number, and active status on regulator site.

- Account segregation: Verify client funds are held in separate accounts from the broker’s operating accounts.

- Clear fee schedule: Confirm spreads, commissions, swap/rollover, deposit/withdrawal fees are published and match your account.

- Deposit/withdrawal paths: Test that your chosen method (bank transfer, card, e-wallet) is supported and review limits.

- Execution model: Ask whether they use

ECN,STP, or market maker, and request typical latency figures.

Two-week testing checklist — important to test in live conditions

- Open a low-size live position and monitor order execution explicitly for two full trading weeks.

- Place

stop-lossandlimitorders and trigger them; confirm fills match expected price or slippage is within published policy. - Execute market, limit, and partial-fill scenarios across peak volatility to test consistency.

- Make a deposit and request a withdrawal; record time-to-complete and any non-obvious charges.

- Interact with customer support at different hours; evaluate response time, competence, and escalation path.

Nice-to-have items — longer-term relationship builders

- Risk management tools: Portfolio analytics,

VaRreports, or Monte Carlo simulation exports. - API & automation: Stable REST/WebSocket access with clear rate limits and sandbox environment.

- Liquidity depth: Level II data or published market depth for the instruments you trade.

- Local client support: A Nigerian payment corridor or local office reduces friction and FX conversion surprises.

- Educational & research access: Proprietary research or quality third-party feeds that match your strategy horizon.

Execution latency: Typical round-trip latency under normal market conditions as claimed by broker.

Reconciliation cadence: How often they provide account statements and trade confirmations.

When testing, keep a simple log: date/time, ticket, expected price, executed price, and support interaction ID. That record is the clearest evidence if issues escalate. For traders who want deeper analysis, services that run Monte Carlo simulations and equity-curve risk reviews can convert these logs into actionable risk limits and position-sizing rules. Trust but verify — these checks catch most costly surprises before they become problems.

📥 Download: Forex Broker Evaluation Checklist (PDF)

FAQ — Evaluating Forex Brokers in Nigeria

Start by choosing a broker that protects your capital, executes trades reliably, and communicates clearly. For Nigerian traders this means checking regulation (local warnings and where the broker is licensed), execution quality, funding and withdrawal routes that work with Nigerian banks, transparent pricing, and customer support during Lagos trading hours. Practical checks—small deposit test, execution screenshots, and a withdrawal trial—often reveal issues no brochure will admit.

Common questions Nigerian traders ask

1. How do I verify a broker’s regulation? Look up the regulator’s public register and confirm the exact legal entity name. Many reputable brokers are licensed in jurisdictions like the UK (FCA), Australia (ASIC), or Cyprus (CySEC); some operate from offshore hubs. Industry analysis shows brokers licensed in strong jurisdictions typically follow stricter client protections.

2. Is it safe to use offshore brokers from Nigeria? Many Nigerians use offshore brokers, but that carries extra risk: limited local recourse and potential currency-transfer friction. Use small test deposits, confirm withdrawal paths, and prefer brokers with reputable international audits.

3. What are the simplest red flags? Unclear legal name or address. Promises of guaranteed returns. * No verifiable live account metrics or negative online reviews piling up.

4. Which trading costs matter most? Spreads and commissions — compare pips and round-turn commission. Swap/overnight rates — relevant for carry/position traders. * Deposit/withdrawal fees — especially for naira conversions and transfer partners.

5. How to test execution and slippage? 1. Open a small live account. 2. Execute market orders during peak volatility. 3. Record timestamps, requested price, and execution price for several trades.

6. What withdrawal issues should I watch for? Delays longer than the broker’s published window, unexpected fees, or requests for irrelevant documentation are warning signs.

7. Are demo accounts useful? Demos are good for platform familiarity but don’t reflect real slippage, fills, or psychology. Always confirm with a small live test.

8. What about customer support? Prefer brokers with Lagos-time coverage, WhatsApp or phone contact, and rapid verification processes.

Segregated account: Client funds kept separate from the broker’s operating funds to reduce counterparty risk.

Negative balance protection: A policy that limits losses to the funded account balance, preventing debt to the broker.

A quick checklist: Do a live withdrawal test. Compare live spreads during news events. * Verify regulatory registry entries.

Choosing the right broker saves time and protects capital; run small, practical tests early and trust real-world trade evidence over marketing claims.

Resource List and Tools

Reliable sources and the right tools cut through noise quickly when building or stress-testing trading strategies. Below are categorized resource types with one-line guidance on why each is useful, followed by a focused table of authoritative links and practical notes for Nigerian traders.

- Regulatory lookups: Use official registers to verify broker licenses and avoid unregulated counterparties.

- Banking & payments: Confirm SWIFT/BIC and local payment rails before moving large sums to reduce settlement risk.

- Market data & execution tools: Real-time feeds and low-latency execution platforms preserve strategy fidelity during volatility.

- Risk & analytics software: Monte Carlo tools and equity-curve analyzers reveal drawdown probabilities and scenario outcomes.

- Local payment processors: Pick providers that support NGN settlement, low FX spreads, and NIN/KYC integrations for smoother onramps.

Organized resource compilation with quick descriptions and use-cases for each link

| Resource | Category | Use-case / Why it’s useful | Notes for Nigeria |

|---|---|---|---|

| FCA register — https://register.fca.org.uk/ | Regulator lookup | Verify UK-authorised firms and view permissions, enforcement actions | Useful when checking UK-based forex brokers used by Nigerian traders |

| CySEC license lookup — https://www.cysec.gov.cy/en-GB/ | Regulator lookup | Confirm Cyprus-authorised investment firms and license numbers | Many European brokers hold CySEC licenses; check retail protections carefully |

| ASIC licence register — https://connectonline.asic.gov.au/ | Regulator lookup | Validate Australian-licensed brokers and company filings | ASIC-listed brokers often service APAC clients; check cross-border terms |

| SWIFT Ref Directory — https://www.swift.com/standards/data-standards/bic | Banking / payments | Lookup BICs and SWIFT directory entries to verify correspondent banking routes | Crucial for confirming international wire rails and correspondent banks for NGN FX settlements |

| Paystack — https://paystack.com | Payment processor | NGN payment collection, low integration friction, inline KYC and settlements | Widely used by Nigerian platforms; supports card and bank transfers |

| Flutterwave — https://flutterwave.com | Payment processor | Cross-border and local NGN collections, payouts, and merchant APIs | Strong African footprint; supports multiple payout currencies |

| Remita — https://remita.net | Payment & bill payments | Government and corporate collections, bulk disbursements in NGN | Common for corporate/utility payments in Nigeria; useful for operational payouts |

Industry analysis shows regulators’ registers and SWIFT checks are low-effort, high-impact steps before onboarding a broker or moving funds. Pair those checks with a payment provider that supports NGN settlement and clear KYC flows to reduce operational friction when funding accounts or withdrawing profits. These resources form the defensive backbone of a practical trade operations checklist.

Conclusion and Next Steps

Start small, test deliberately, and treat each trade idea as an experiment. Over the next few weeks, the focus should be on converting hypotheses into measured results: a tight action rhythm, clear allocation rules, and consistent documentation will turn noisy market moves into usable edge.

- Identify and backtest one strategy variant to test over a 4-week window.

- Allocate capital for live testing using a staged sample approach (see allocation guidance below).

- Record every trade outcome in a comparison matrix and run a simple evaluation at the end of each week.

- Choose the variant: pick one timeframe (e.g., 1-hour EUR/USD mean-reversion) and a clearly defined entry/exit rule. Run a quick historical check (30–90 trades) and note expected win rate and average return per trade.

- Paper-trade or micro-live for Week 1–2 to verify assumptions. Use Week 3–4 to scale up only if performance is consistent.

- End of Week 4: run a simple statistical check — compare realized metrics to the backtest and decide to continue, tweak, or pause.

- Stage 1 — Proof of concept: 0.5%–1% of deployable trading capital; position sizes small enough that a single loss is immaterial.

- Stage 2 — Validation: increase to 1.5%–3% per active strategy once two consecutive weeks match expectations.

- Stage 3 — Scale: up to 5% per strategy only after a month of validated performance and acceptable drawdown behavior.

Short-term plan details and timelines

Sample allocation for testing

Practical tips for allocation: use max_drawdown_limit = 0.03 as a guardrail (stop increases if equity drawdown exceeds 3% during the test window). Adjust percentages to your risk tolerance and total capital.

Documenting outcomes: comparison matrix

- Trade ID: unique identifier per trade.

- Setup: brief description of rules that produced the entry.

- Size & allocation: capital used and percent of equity.

- Result: P&L, duration, slippage.

- Notes: deviations, market conditions, emotional factors.

Log each field consistently. At week-end, filter the matrix for patterns — time-of-day edges, recurring slippage, or execution gaps.

If more rigorous evaluation is desired, use a Monte Carlo resampling on realized returns; this helps estimate variability before scaling. For Nigerian traders facing volatile local FX or equities, prioritize execution quality and slippage tracking — a good idea executed poorly will still fail.

This plan keeps decisions data-driven and reversible, turning intuition into repeatable process. Stick to the cadence, keep the matrix honest, and let the results guide whether to iterate or scale.

Conclusion

Trustworthy brokerage choice comes down to a handful of practical checks you can run today: confirm regulation and withdrawal history, test execution and order types on a small live or funded demo account, and compare total trading costs—not just headline spreads. Earlier examples showed brokers with attractive spreads but repeated withdrawal delays, and others with higher commissions yet consistently tighter execution; those patterns make clear why priority should be liquidity, execution quality, and real withdrawal experience, not marketing pages.

If you’re unsure where to start, take these next steps: – Open a small verification account to test deposits, withdrawals and support. – Run execution tests during news hours to observe slippage and fills. – Compare true costs using the cheat sheet and sample broker matrix from this article.

Want a practical walkthrough or curated broker shortlist tuned for Nigerian traders? Resources like NairaFX broker guides can help streamline verification and match options to your funding method and risk profile. For most traders the sensible move is incremental: verify, trade small, then scale with the broker that proves reliable under stress.