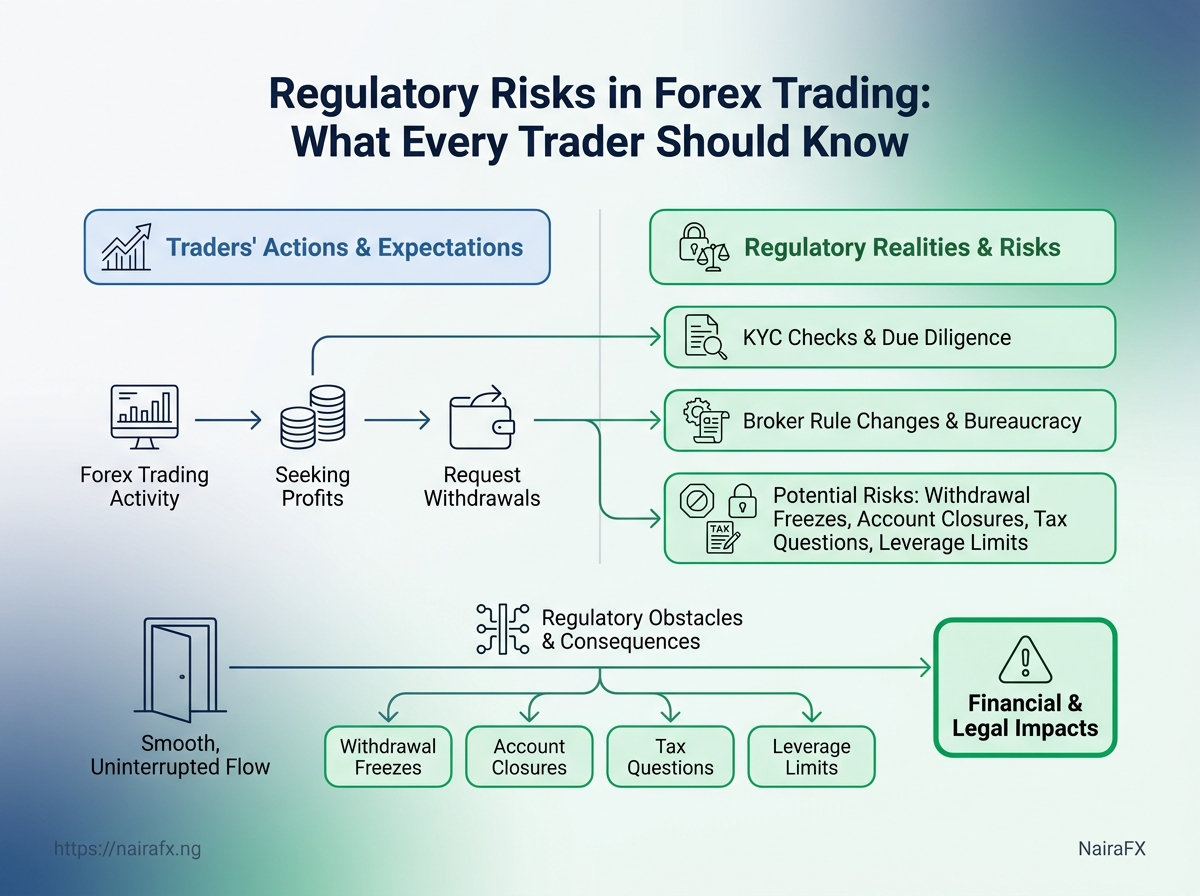

A profitable trade can turn messy fast when a broker changes the rules, freezes a withdrawal, or closes an account without much warning.

That is where regulatory risks in Forex trading become real.

They are not just legal fine print; they shape who can trade, how much risk is allowed, and whether money moves smoothly when it matters most.

Forex trading regulations differ by country, and that matters for traders in Nigeria and beyond.

A broker that looks attractive on spreads or bonuses may still create problems through weak oversight, vague terms, or poor client protection.

The hardest part is that trading compliance risks often show up after the trade looks successful.

A trader can enter with a solid plan, then run into KYC checks, leverage limits, tax questions, or account restrictions at the worst possible time.

That is why regulation should never be treated as background noise.

It affects safety, access, and the long-term health of a trading account just as much as entry timing or chart analysis.

Quick Answer: Regulatory risk in forex trading is the chance that a broker’s authorization status, compliance process (KYC/account restrictions), or withdrawal handling can limit access to your account or block withdrawals—even when your market trades are otherwise normal. To reduce this risk, don’t rely on marketing or a “regulated” badge. Use the broker-type safety breakdown (Section 5) and the pre-funding terms checklist (Section 8), then complete a small withdrawal test after verification clears (expanded in Section 11 for Nigerian-specific pressure points).

What Regulatory Risk Really Means for Forex Traders

Have you ever seen a trade setup look perfect, only to realize the bigger risk sits outside the chart?

That is regulatory risk.

It is the chance that broker rules, licensing issues, account restrictions, or compliance changes damage your trading results even when price behaves normally.

Regulatory risks in Forex are not the same as market risk.

Market risk comes from candles, spreads, and volatility.

Regulatory risk comes from the rules around how you enter, fund, hold, and withdraw from a trade.

For Nigerian traders, this matters even during quiet market sessions.

A calm market does not protect you from a broker freeze, a payment disruption, a sudden policy change, or a platform that stops serving your region.

Those are trading compliance risks, and they can hurt faster than a bad entry.

A simple way to think about it: market risk affects your trade; regulatory risk can affect your access to the trade itself.

- Broker licensing: A broker may look polished but still operate with weak oversight or unclear authorization.

- Account access: Rules can change how you open, fund, or keep an account active.

- Withdrawal delays: Compliance checks can slow or block payouts, even when your trade was profitable.

- Product restrictions: Leverage limits, bonus bans, or symbol restrictions can change your trading plan overnight.

Nigerian traders should care because the local context adds another layer.

Payment rails, cross-border transfers, and broker policies can shift without warning, and that can turn a normal trading week into a messy one.

A trader who ignores regulation often discovers the problem late, usually after deposit, after profit, or after a dispute.

A trader who checks it early protects capital before the first position opens.

That habit is part of serious Forex trading regulations awareness.

It does not make trading less exciting.

It makes the business side far less expensive.

Keep the chart on one screen and the broker rules on the other.

Both decide whether a trade is truly worth taking.

The hard truth: not every broker is playing by the same rules

A polished website can hide a weak license.

That is the uncomfortable part of Forex trading regulations: two brokers may look similar on the surface, yet their rules, oversight, and client protections can be worlds apart.

Licensed brokers usually answer to a real regulator, file complaints processes, and follow conduct rules.

Offshore brokers may still be legitimate, but their supervision is often lighter, and unregulated platforms sit in a far riskier zone for trading compliance risks.

The practical test is simple.

Can you verify the legal entity, the license number, and the regulator that can actually act if something goes wrong?

Broker types at a glance

| Broker type | Typical regulation status | Client fund protection | Withdrawal risk | Common red flags |

|---|---|---|---|---|

| Tier-1 regulated broker | Licensed by a top-tier regulator such as FCA, ASIC, CySEC, or NFA/CFTC where applicable | Segregated client accounts, stricter reporting, and stronger complaint routes; some jurisdictions add compensation or negative balance protections | Lower, provided the account matches the licensed entity and KYC details are clean | Missing license number, vague company name, pressure to deposit fast, unclear complaint process |

| Offshore broker with limited oversight | Registered under a lighter regime, often with weaker enforcement and fewer investor remedies | May promise segregation, but supervision and dispute recovery are usually weaker | Moderate to high, especially when bonus terms or extra checks delay payouts | No local legal presence, bonus-heavy terms, unclear fees, limited regulator contact |

| Unregulated platform | No valid brokerage license, or only a basic business registration with no meaningful market supervision | Usually none beyond the platform’s own promises | High, with little recourse if funds are blocked or denied | No license, no real address, crypto-only deposits, copied terms, unverifiable testimonials |

It normally requires the broker to keep client money separate, publish legal disclosures, handle complaints, and meet ongoing conduct rules.

- Segregated funds: Client cash should sit apart from company operating money.

- Clear legal identity: The regulated entity, not just the brand name, must be visible.

- Complaints pathway: A real regulator or ombudsman route should exist.

- Disclosure rules: Fees, execution model, and risk warnings should be plain.

- Ongoing supervision: The firm should face reporting, audits, or capital checks.

The biggest warning sign is opacity.

If the broker hides its license, buries the entity name, or leans on bonus language, the supervision is probably thin.

That is why broker due diligence matters before the first deposit.

In this part of the market, the paper trail often tells you more than the sales pitch.

A trader’s story: losing money before the market even moved

On Monday, the account looked clean.

The trades were small, the spread was fair, and the balance even ticked up a little.

By Friday, the trader was not fighting price at all.

The problem was a withdrawal request that sat untouched, then a support reply asking for more documents, then silence.

That is how trading compliance risks show up in real life: not as a dramatic loss on the chart, but as cash that gets stuck when the broker starts asking questions.

What slipped past during onboarding

The trader had opened the account quickly and treated the forms like a chore.

That usually means the same things get skipped: bonus terms, withdrawal rules, identity checks, and the fine print on who can trade from which country.

With Forex trading regulations, the dangerous part is not always the rule itself.

It is the moment a broker decides the account does not match its onboarding record, and the withdrawal turns into a compliance review.

- Identity details: A mismatch between the name on the account and the payment method can trigger delays.

- Funding source: Some brokers want deposits and withdrawals to come from the same channel.

- Country restrictions: A trader may pass sign-up, then hit limits later because the jurisdiction was never supported.

- Document timing: Expired IDs, blurry selfies, or missing proof of address can stall a payout.

The first questions we ask when a broker gets difficult

If a broker becomes slow, the first move is not panic.

It is evidence.

Save every email, chat log, screenshot, and transaction reference before the trail gets messy.

Then ask simple questions:

- What exact rule is being applied?

- What document is still needed?

- Was the withdrawal method allowed at signup?

- Is the account under review for verification or fraud controls?

A trader can survive a bad entry.

Losing access to funds before the market even moves is harder to forgive.

That is why the real habit is simple: read the onboarding terms like they matter, because they do.

Surprising stat: the fine print often matters more than the headline promise

Why does a broker’s best-looking offer sometimes become the worst trade you never took?

Because the contract usually hides the real rules.

The headline may talk about tight spreads or a welcome bonus, but the legal pages decide what you can actually do, how fast you can withdraw, and when your account gets restricted.

That is where trading compliance risks start showing up in day-to-day trading.

The sharpest surprises usually sit in four places: contract clauses, margin or exposure limits, bonus terms, and fee disclosures.

A clause can ban hedging, cap position sizes, or allow the broker to change conditions during extreme volatility.

Bonus terms can lock withdrawals until turnover rules are met.

Fee pages often bury inactivity charges, swap costs, conversion fees, and withdrawal fees in plain sight.

Hidden restrictions rarely announce themselves.

They show up when an order is rejected during news, when a withdrawal request stalls, or when the platform quietly cuts your available exposure after a balance change.

For anyone comparing Forex trading regulations across brokers, the practical question is not just who is licensed.

It is whether the client agreement gives you fair access once you fund the account.

Pre-funding review checklist

| Check item | What to look for | Why it matters | Pass or fail |

|---|---|---|---|

| Regulator name and license number | The exact legal entity, regulator, and license number should match the public register | Confirms the broker is actually authorized under the stated jurisdiction | Pass if the register matches exactly |

| Client fund segregation | Client money should be held separately from company operating funds | Reduces the risk that company trouble affects client balances | Pass if segregation is clearly stated |

| Withdrawal policy | Look for processing times, approval steps, minimum amounts, and identity checks | Prevents delays and surprise blocks when you want your money out | Pass if terms are clear and specific |

| Negative balance protection | Check whether the broker covers losses below zero and in which regions | Matters during fast moves and gaps, especially around news events | Pass if coverage is clearly written |

| Complaint process | The agreement should name the complaint channel and escalation route | Gives you a path if a dispute starts over fees or execution | Pass if the process is documented |

| Bonus turnover rules | Read how many lots or trades are needed before withdrawal | Bonus terms can trap funds longer than expected | Pass if the rule is simple and realistic |

| Inactivity fee clause | Look for monthly charges after a quiet period | Small accounts can be drained by silence, not trading | Pass if the fee is low and disclosed |

| Execution restrictions | Check for limits on scalping, hedging, or news trading | These are common sources of account disputes | Pass if the rules match your style |

A risky one leans on vague phrases like “at our discretion,” “subject to review,” or “unusual market conditions,” then uses those phrases when money moves.

The real test is simple: if a rule changes how you trade, withdraw, or manage risk, it belongs on your checklist before funding the account.

That is how the fine print stops being an afterthought and starts becoming part of your risk control.

Contrarian take: the safest-looking broker is not always the safest choice

A broker with the cleanest website can still be a poor place to keep serious money.

In Forex, surface trust is not the same as legal protection, and that gap is where many traders misread risk.

Jurisdiction matters more than polish.

A broker regulated in one country may offer a compensation scheme, a hard complaints path, and real enforcement power; another may only have a registration number and a nice badge.

That difference sits at the heart of Forex trading regulations and the real trading compliance risks traders face.

Price matters too, but not first.

A tighter spread is nice, yet it means very little if the broker sits in a weak jurisdiction, has no clear complaint channel, or can change terms without meaningful oversight.

Comparing broker safety the right way

| Do | Don’t | Better question to ask | Why it matters |

|---|---|---|---|

| Check the regulator on the regulator’s own database | Trust a homepage badge or footer logo | Is this firm actually licensed where it says it is? | Confirms whether the broker is accountable |

| Look for a named compensation scheme | Assume every regulated broker offers compensation | If the broker fails, who pays and up to what limit? | Protects client balances when a firm becomes insolvent |

| Read the complaints process before funding the account | Assume support chat is a real complaint channel | How does a client submit a formal complaint, and who reviews it? | Shows whether disputes have a formal path |

| Compare the legal entity, not just the brand name | Treat the marketing name as the regulated firm | Which company holds my account contract? | The legal entity determines which rules apply |

| Review leverage limits by jurisdiction | Chase the highest leverage first | What leverage is allowed here, and what risk does it add? | High leverage can magnify losses fast |

| Check withdrawal terms carefully | Focus only on spreads and bonuses | Are withdrawals restricted, delayed, or conditional? | Safety is useless if you cannot access funds |

| Test platform features after regulation checks | Pick a broker for charts and indicators alone | Do the tools justify weaker protection? | Features do not replace legal safeguards |

| Read negative client reviews for patterns | Dismiss all complaints as noise | Are the complaints about withdrawals, slippage, or account closure? | Repeated issues often point to control problems |

A broker with average spreads and solid supervision is usually a better choice than a cheap-looking broker with thin oversight.

That trade-off matters even more in volatile markets.

The best fit is often the one that balances legal protection, clear complaint routes, and acceptable costs, not the one shouting the loudest about low fees.

The safest-looking broker is not always the safest choice.

In Forex, real safety comes from where the firm is based, how it is supervised, and how easily a trader can enforce a claim.

What happens when you trade from Nigeria but compliance risk still creeps in?

Even if a broker “looks regulated,” the real question for Nigerian traders is whether its compliance process stays smooth with the way Nigerians typically fund and withdraw (bank transfers, cards/payment processors, and cross-border rails).

You already have a pre-funding checklist above—so this scenario is about the Nigeria-specific pressure points that usually trigger account reviews when deposits or withdrawals are about to happen.

The Nigeria-focused screening questions (before you scale up)

- Does the contracting entity match the payment channel you’ll actually use?

- Are Nigerians supported on the exact funding/withdrawal method you plan to use?

- What documents does the broker expect from Nigerian traders (and how strict are they)?

- Does the broker have a clear path for dealing with compliance reviews from Nigeria?

Do a small “withdrawal test”—but test the right thing

Yes, start with a small live account. But also test withdrawal conditions.

- Deposit using the same method you intend to withdraw with.

- Request withdrawal as soon as basic verification completes.

- Watch for conditional triggers (turnover tied to bonuses, extra ID checks, payment-rail re-validation).

If withdrawal access is delayed or repeatedly re-verified, treat that as compliance risk—not “bad luck.”

When you need escalation, keep it structured (not emotional)

You don’t have to argue with support—you have to make the review actionable.

- Request the exact reason code/policy cited for the delay (what rule they’re applying).

- Ask what one document or step will complete the review (avoid “submit everything” loops).

- Keep a short timeline of: date/time, withdrawal reference/ticket, what support requested, and when you resubmitted.

If support cannot tell you what rule is being applied—or the timeline keeps moving with no checklist—pause trading growth until the compliance path is clear.

A broker doesn’t need to be perfect for Nigeria trading, but it must be traceable, consistent, and responsive when money is moving.

What are the CFTC priorities for 2026?

The article does not list any specific CFTC priorities for 2026. What it does emphasize is that regulatory priorities typically translate into stricter enforcement around broker licensing, KYC/compliance checks, and withdrawal or account-access handling. To stay prepared, verify the latest CFTC releases and any updates affecting forex broker oversight and retail account rules.

Is forex regulated by CFTC?

Forex regulation is jurisdiction-dependent, and it may fall under CFTC oversight for certain forex-related products and broker activities in the United States. The key practical takeaway is that traders should confirm whether their broker is authorized by the relevant regulator before funding, because weak oversight can lead to KYC/account restrictions or delayed withdrawals. Always verify the regulator/authorization status and read withdrawal and account terms.

Who is MiFID II applicable to?

MiFID II generally applies to investment firms, trading venues, and other regulated entities that provide or facilitate financial services in the EU/EEA. The article’s core point is that different regulatory regimes create different protections and enforcement strength, which can directly affect how brokers handle onboarding, compliance checks, and payouts. If you trade under MiFID II coverage, confirm your broker’s EU authorization and dispute/complaints pathway.

What is the minimum capital requirement for CFTC?

The article does not provide a minimum capital figure for CFTC-related requirements. In practice, minimum capital depends on the type of registrant and the applicable CFTC/NFA rule set, so using a single number without verifying the exact registration category can mislead you. Check the current CFTC and NFA requirements that match your broker’s registration status.

What are the new rules for CBN 2026?

The article does not state any new CBN rules for 2026. Since regulatory changes can affect deposit/withdrawal compliance, account access, and documentation requirements, you should monitor official CBN circulars and forex-related guidance before relying on a broker’s payment flow. This helps reduce the risk of cash getting stuck when compliance checks tighten.

The Broker Rulebook Matters More Than the Chart

The biggest lesson here is simple: a trade can be right and still go wrong if the broker’s rules are weak, unclear, or unevenly enforced.

That is why regulatory risks Forex traders face deserve the same attention as entry points and stop losses.

In practice, Forex trading regulations are not background noise; they decide whether your money can move smoothly when you need it most.

The trader who lost access before the market even moved is a good reminder of what trading compliance risks look like in real life.

A polished website and a tight spread mean very little if withdrawals stall, account terms shift without warning, or dispute channels go nowhere.

Safety is not just about looking regulated; it is about being able to verify the licence, read the fine print, and trust the process when pressure hits.

Check the broker before the next trade. Start with the licence, then read the withdrawal terms, bonus rules, and complaint process with a colder eye than you use for the chart.

If that feels tedious, good — that caution is often what keeps a small problem from becoming an expensive one, and our risk-focused guides at NairaFX can help you evaluate the next step with more confidence.